Experian Offers Higher Credit Scores for Access to Bank Accounts.

Your Credit Minute Show Notes:

00:01 What’s up everyone. Nik Tsoukales here with Key Credit Repair. I’ve got some quick credit news for you, hot off the press from Housing Wire uh, yesterday morning. Um, we have Experian offering potentially high credit scores in exchange to access to people’s bank accounts, and a lot of people are wondering what this is all about. And a lot of people are wondering about some other news, that kind of coincides with this about having cell phone usage, or how you’re paying your cell phone, uh, affect your credit in a positive way.

00:28 So, in the past, what has always happened was if you’ve made your uh, utility payments on time, um, including your cell phone payments, it didn’t report to the credit agencies. But, if you wanted to default, it quickly reported as a collection. It’s probably the number one thing that we work on here at Key Credit Repair. But, you never got the positives from it, only the negatives if things fell apart. Well, Experian today, or yesterday, uh, announced that it’s releasing a new program called Experian Boost. Kind of an interesting little uh, little program. How beneficial it’s going to be, um, kind of up for debate, because it’s only Experian’s program. Obviously, we want to see all three credit agencies, and all three credit scores looking good. Experian, Trinity and then Equifax. But even so, this is a step in the right direction.

01:12 So essentially, what’s going to happen is you’re going to be providing Experian, and obviously this is an opt-in, you’re going to be providing Experian with your bank account information. Experian will then use some fancy software to log into your bank account and essentially analyze your transactions and look at things like utility payments, okay? They will then report those on-time payments to your utility companies, as well as your cell phone company, um, to uh, the Experian credit report. That will then get taken into account under their new FICO eight algorithm, and will potentially increase your credit scores.

01:45 Now, let’s say you’re not making a cell phone payment, or let’s say you stopped. You get a late. That’s one of the questions we’ve been asked today about this, and the answer to that is right now, probably not. What they’re telling us is if you stopped making a payment, maybe a payment’s not due, um, what’ll happen is if you stop making those payments, 90 days later the Experian Boost program simply will not take that account, uh, will not take that account into account. So, it will no longer report to uh, the Experian credit report, so keep that in mind. So, you shouldn’t be negatively affected. Obviously, if you miss payments for 90 days, it will then go into collections anyway, so you’ll get the negative ramifications of that then.

02:26 Um, some quick stuff. This is uh, for utility bills. Um, cell phones. Again, uh, if you stop paying, it will discontinue in 90 days. This is being used for FICO eight. Keep in mind, banks and lenders, for the purpose of mortgage lending, they’re not using FICO eight. They’re using FICO four. They’re using some prehistoric versions of the FICO algorithm. FICO eight is not the score of choice for home lending. And I say this, and I, and I warn everyone, because this is the credit score that our typical client is using to finance a home. Um, most of our clients are trying to buy a home eventually. They’re trying to become uh, homeowners from lenders, so it’s very important.

03:06 Um, also something to keep in the back of your mind is the fact that you are linking up your bank account information to Experian. Not to say that al-, already have everything on us, uh, they already have a lot of our data, but you’re also linking up your bank account information. So, they’ll have the ability to see uh, your spending habits, and where your money’s going, so that’s something to think about as well. Do we want to share that aspect of our finances with one of the credit agencies? We all know the credit agencies do resell data, okay? They’re big marketing company as well, so that’s another thing to keep in mind. Uh, guys, this is Nick Tsoukales with Credit News Daily. I’m going to include a link here for the text, or transcript of this blog. Feel free to read through it, and feel free to email us at info@keycreditrepair.com. If you have any questions on how this could adversely affect you, or even benefit you in the future. Thanks and have a great day.

Experian offering potentially higher credit scores in exchange for access to people’s bank accounts.

What is the Best Way to Manage your Credit Card Spending?

Your Credit Minute Show Notes:

00:00 Hey guys, credit question of the day coming from [Shanta Clark 00:00:03]. Thank you so much for sending us this message, um, and for giving us this post. So- so Shanta asked, “What’s the best way to manage your credit card spend?” Guys, the best way to manage it is to not use them. Call me old school. I’ve met a lot of rich people in the last 10 years and the general consensus is cash is king. Spend all the money in your pocket. Budget all you want, but if you can’t budget, don’t worry about it.

00:28 Save some money every week out of your paycheck. Um, and then if you wanna burn through everything else, burn through. Have fun spending it. Have a ball, okay? Let’s stay away from credit card debt. There shouldn’t be credit card spending. There shouldn’t be, uh, any credit card spending management. That shouldn’t be a tool. It shouldn’t be in system … It shouldn’t be a system. If you’re caught up in the points game, you’re dead in the water already guys.

00:52 So again, my suggestion … Um, Shanta Clark, again, thanks for your question, but my suggestion is stay away from the whole darn thing. It’s the number one wealth buster in the United States.

What’s the best way to manage your credit card spending?

How much money to save in case of an emergency?

Your Credit Minute Show Notes:

00:00 All right guys. Credit question of the day. And we’ll actually make this a finance question of the day, is coming from [Sherry Lynn White 00:00:06]. Sherry Lynn thank you so much for posting your question on our Facebook page and the question is: How much money should you save in case of an emergency? Well, let’s think about this. In 2008, I would have said a year’s worth. Why? Because when people lost jobs in 2008, it took a lot longer to get a job. Now, the economy is a little stronger, if you’re going to apply for another job, it might be a shorter time frame. So, I would say the minimum should be six months. Okay. You want to look at all of your monthly expenses, you should be able to jot this down on a small piece of paper, even a napkin. Jot down those expenses, times six, that’s what you want to have in the bank. Now, if you’re getting out of debt, I would suggest actually putting that to the side. Okay. The debt’s probably costing you 20 plus percent, get a $1,000 in the bank, just in case of an emergency, something breaks down, you got a car issue, you need to rent a car, something happens. Okay. And attack the debt, don’t worry about your reserve.

01:03 SO the order is, put a thousand bucks in the bank, pay off the debt, and then move to get six months reserves. And once you’re done with the six months reserves, then you want to start investing in putting money into retirement. Thanks, guys. Have a great day.

How much money should you save in case of an emergency?

Should you Pay off Debt Slowly or all at Once?

Your Credit Minute Show Notes:

00:01 Marlena Perkins, thank you for your credit question on our Facebook page earlier. And Marlena’s question is, “This would be a blessing. Is it better to pay off debt slowly or all at once?”

00:13 Okay. Real simple, guys. It’s just the numbers. If you’ve got the money in the bank, it’s earning .0015%, like literally nothing. Okay? Your money, uh, if you compare it to, or if you compare the interest rate you’re getting from the bank to the inflation, your money’s actually losing value in the bank. Your credit card company’s charging you 28%. Right?

00:36 So, your money’s sitting in the bank is costing you 28%. Okay? If you’re nursing credit card debt. So, should you pay it off at once if you have the money? Absolutely. Hell, yes. You better do it. Um, you will be fine if you want to leave $100.00 in your pocket just in case something happens between now and the next paycheck. Rock and roll, but pay off the debt. Don’t nurse it. It’s not your friend. Credit card companies don’t like you. They’re trying to get paid by you. Okay. So, get away from debt. If you need to pay it slowly, then what you want to do is start with the smallest debt, pay the minimums on everything else. Pay that sucker off and move your way up the list. It’s called the Snowball Effect, but we can talk about that another time.

01:16 Have a great day, guys.

Is it better to pay off debt slowly or all at once?

Is it Okay to only Give the Minimum Payment on My Credit Card?

Your Credit Minute Show Notes:

00:00 All right, guys. Credit question from Paige, Paige Majelki. I’m sorry if I butchered your name, Paige, and the credit question of the moment is, is it okay to only pay the minimum payment on my credit card? And, I’m going to give you- I’m going to- I’m going to use a curse word. Hell no.

00:19 Guys, if you’ve read the disclosure, if you’ve read your credit card bill, you’re going to see there’s a little disclosure box that shows how much you will pay back and how long it will take you to pay off a credit card, um, if you only pay the minimum payments. And, you know what the average is ladies and gentleman on a $2,000 credit card? 18 years. 18 years because you bought a coat. That’s insane.

00:45 So, the answer is hell no. Even if you have to send in a dollar extra, you need to do it guys. You cannot maintain these balances. You- You cannot send in the minimum. You can’t nurse these things. They’re not your friend. If you have too many credit cards or you have to list them out on a spreadsheet, you’ve got a problem. You cannot organize credit card debt. It’s debt. It’s the devil. Get away from it ASAP.

Is it okay to only pay the minimum payment on my credit card? (Curse words)

The Best Way to Manage your Credit Card Spending?

Your Credit Minute Show Notes:

00:00 All right guys, awesome credit question. What is the best way to manage your credit card spending? You want to know the best way? Don’t use them. It sounds insane. Guys, you just don’t use them. Carry cash. I know it sounds insane. You want to spend all the money in your pocket, rock and roll.

00:20 I’m not a believer in budgeting, okay? When you get paid, put some money aside. Everything else, if you want to burn through it, burn through it. Guess what? If you’ve simply burned through the money in your pocket and haven’t accumulated debt, you are doing better than the average American that’s got about $14,000 per household or some absurd number that keeps going up on a consistent level. Stay away from it. Don’t use it. You don’t need it.

00:44 If you feel like you can’t avoid the temptation, I would say, I wouldn’t say close out the credit cards. Um, if you’ve seen some of my previous videos, I’m going to teach you a little hack. Take those credit cards, stick ’em in a cup, a red cup. Everyone’s got a red beer cup at their house. Stick ’em in a cup, fill the cup up with water, stick that sucker in the freezer.

01:02 You think I’m insane? Think about the psychology. You find something shiny. You want to buy it, okay, but you can’t because you don’t have the credit card on you. Or maybe you’re just using your cash, so be it, that’s fantastic. Use your cash, but let’s say you don’t have enough. You need your credit card. Well, guess what? You gotta leave the mall, you gotta drive home, you gotta walk into your kitchen. Everyone’s yelling at you, the kids are yelling, it’s, it’s, it’s a busy house. You’ve probably forgotten about your purchase, and if you haven’t, you gotta go into the freezer, take this cup out of the freezer, stick it on your counter, and wait for it to melt.

01:36 How silly do you feel doing this? Well, guess what, in feeling silly about this, you might, number one, change your mind, okay? Also, time will pass. It’s gonna take a day or so for that thing to melt, right? Time will pass, you’ll get busy, and you’ll probably see something else that’s shinier, and you might just forget about it, okay? Compulsion has, uh, an expiration, and it’s usually about six to 12 hours, okay, so if you can get through that compulsion period, um, you can make a more educated decision. If you really want it at that point, again, I don’t recommend buying it, whatever you need on the credit card, but at least you had given yourself a chance to think about it, guys, so see ya later.

What is the best way to manage your credit card spending?

Should you Pay for an Item that is in Collections?

Your Credit Minute Show Notes:

00:01 What’s up, guys? This is Nik Tsoukales with Key Credit Repair. Um, we posted an awesome raffle this week just asking you to post your questions, so one lucky winner this week is going to get a $250 American Express gift card and all you have to do is post your question, so please continue.

00:16 So, one of our questions that we got from Teresa Walker-Woodroth, and excuse me as I’m reading off my screen is, “If an item is in collections, should you still pay it?” So, let’s actually peel the onion back just a little bit more. If it’s something that’s questionable, if it’s something that’s old, if it’s something that’s past the statutes of limitations, which could be anywhere between 10 or as low as, uh, uh, three years in the state that you live in, you might not want to. You might want to challenge the record. You might want to request validation of the record to ensure if you’re gonna pay it, you’re paying off the right person, you’re paying the right amount, uh, and really that it’s just not an invalid debt.

00:55 Also, if the debt does come back as validated, keep in mind that if it’s with a debt collection agency and the debt collection agency is doing all the right things and you do want to pay it, it doesn’t mean you can’t negotiate a settlement. So, let’s say the, the, the collection agency has bought the debt for ten cents on the dollar, there’s nothing that stops you from offering them twenty cents on the dollar. They still make a little money and you get a discount. You can get a lot of the junk fees waived off of the collection amount. Um, and you can get rid of the debt. Now keep in mind, paying off the collection doesn’t necessarily remove the record. In fact, most of the time, it does not remove the record. But it’s still a step in the right direction if you feel like the debt is a valid. If you want to work on removing the record post paying it, then it’s something we can have a conversation about.

01:41 Thanks, guys. Nik Tsoukales with Key Credit Repair. Again, thank you to Teresa Walker-Woodroth for posting this awesome question. Have a great day.

If an item is in collections should you still pay it?

Can you be Charged for Closing a Credit Card?

Your Credit Minute Show Notes:

[00:00] All right. This credit question is coming from Wendy Rush. Um, she posted on our Facebook page a couple days ago, and I like this question, and you might not like the answer. So, I’m going to read this off. How can a credit card company charge you to close out a credit card if it’s already paid off? If that makes sense. It makes a ton of sense, and I want to remind everybody that when you sign up for a credit card, the disclosures, although they’re digital, and you don’t- no one reads the room, you just check the box. They’re probably about this thick if you were to print them out. Okay. So, keep that in mind.

[00:33] There are all types of hidden fees. Although, credit card companies just like any financial institution, they are regulated, they are not in favor of the consumer. There’s a reason where if you sneeze the wrong way, you’re getting charged a fee. The interest rates going up. The reason- There’s a reason why credit card debt is so prevalent in the United States because the balance is grow, grow, grow, and fees accumulate, accumulate, accumulate. So, keep that in mind. It’s not a fair system, but it does sure happen, guys. Thanks.

How can you be charged for closing a credit card?

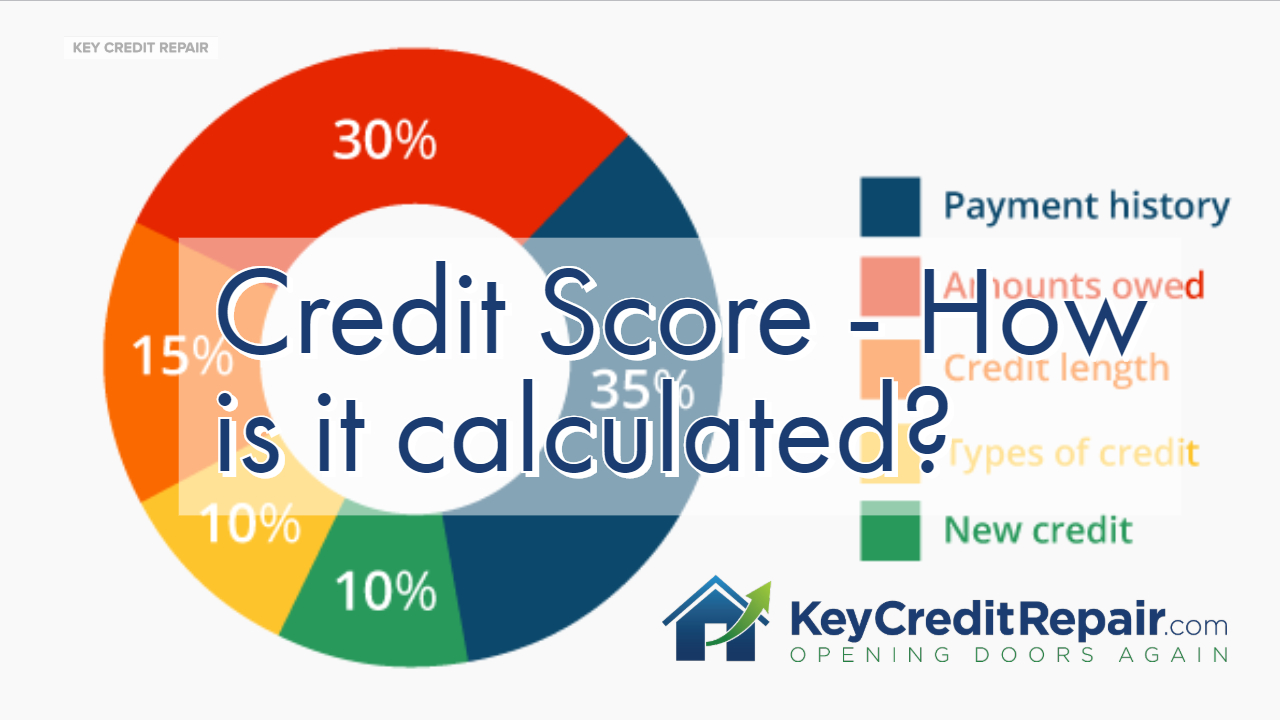

How is Credit Score Calculated?

Your Credit Minute Show Notes:

00:01 Awesome credit question, guys, from Lori Magelky, Lori Magelky, nice to meet you, Lori. Um, and her, her question is real simple. How is a credit score calculated? So, guys, I’m actually going to pull this up and show you how it’s calculated. Okay. There are five parts. We call these the FICO 5 and if you simply just Google “FICO scores” and you click the images button, which is exactly what I’m doing right now, you’re going to see what makes up the credit score. Okay. So we have, let’s actually document this for you. We’re going to erase my pretty house.

00:39 So, the FICO 5 is going to consist of … we’ve got 30%, actually 35%, we have pay history, guys. Okay? 30% is debt. Then we have 15% length of history. Then we have 10% credit mix. And then another 10% for new credit. Now, let me elaborate a little bit on these numbers. Let me move to the side so you can see them. The first one is payment history. 35% of the score is just payment history. Anytime you get a 30 day late, guys, it’s going to effect your credit score in a negative way. Okay? That’s going to effect the 35% of your credit score. Okay? Uh, of what makes up your credit score. Any time you make a payment on time, okay? It’s due on the first, you made it on the first. It’s due on the first even if you made it on the fifth, it counts as an on time payment. You’re getting the great credit for it. Okay? So on time payments are number one.

01:41 The second thing is amounts owed. This is the big flop for a lot of, um, for a lot of our clients. Okay? Specifically the amount you owe in proportion to the credit limits on credit cards. Having past due balances and having items in collections. The amounts you owe is 30% of what makes up your score. So, for those of you that have never missed a payment on time, or excuse me, have never missed a payment, you’re paying everything perfectly for 50 years but you’re maxed out on your credit cards, you’re going to take a hit here. Okay?

02:10 The next 15% is the length of credit history. How old your accounts are. Older people tend to have higher credit scores. Why is that? Well, because their accounts tend to be older. Okay? Age does not go into the credit score but the age of your accounts certainly do.

02:27 Beyond that we have 10% which is new credit. When you get credit, people want to give you credit. Okay? Do you ever get approved for a credit card and then all of a sudden you get five new flyers in the mail for five new credit card offers that are even better than the one you just got? The reason for that is that inquiry is registered. That new account that hits your credit report is registered and you get a bump in your score. And all of a sudden you get more credit offers, guys.

02:52 And last but not least we have credit mix. This is a big one. Okay? Although it’s only 10%, it’s an easy opportunity. Some of you only have student loans. Some of you have only had a mortgage. Some of you only have credit cards. Those are the three types of accounts. Mortgage or real estate related, revolving, and installment. Okay? You want to have a mix of all of that. You don’t just want to have credit cards or mortgages or installment or two out of the tree. The ideal mix is one of each. Okay? The number of accounts isn’t as relevant as the mix of the different types of accounts.

03:26 So, guys, thank you again. Um, big thank you to Lori Magelky for that awesome question. And if you have any additional questions, obviously, hit us up directly at keycreditrepair.com. See you, guys.

Credit Score – How is it calculated?

Credit Repair – How Do I Start?

Your Credit Minute Show Notes:

00:00 What’s up guys? Nik Tsoukales here with Key Credit Repair. Another great question we got … I’m going to read this actually right off our Facebook, um, post. Yvonne Drummer is asking, “How do I start to fix my credit?” Well, the way you start is by pulling your credit report, okay? This is half the battle. We get a lot of people that think their credit is a lot worse than it is because they’ve been hiding from their credit for so many years. And then we pull it and find that half the stuff they thought that was there is just not there. Okay?

00:28 Also, when you look at the data, immediately your brain will start to formulate a plan, even without Key Credit Repair, even without Nick, even without my team, you will begin to formulate a plan almost automatically by just simply looking at the credit report, okay? Put together your own plan, look at your own credit report, and then if you feel like you’re out of luck, you’re not sure how to handle it, then you can reach out to a professional agency that can help you formulate a more in depth plan. But the way you start is by starting. Pulling the credit report. Credit Karma, annualcreditreport.com, PrivacyGuard, there are a million and one websites. Just make sure that you’re getting all the data from all three bureaus and some sort of score, whether it’s a FICO four, five, eight, whether it’s a VantageScore, as lon as it’s a score that can gauge where you are, you know, in the rankings and the grand scheme of things and it can give you kind of an A, B, C, D or F grade, you’re in great shape, but again, recap, just get started.