00:00 What’s going on guys? This is Nik Tsoukales from Key Credit Repair. Um, thank you for checking out our channel.

00:05 So, question of the day is a pretty common one; “Why are my credit scores different for the three credit bureaus?”

00:11 And I’ll give you an example, and you’ve probably seen this yourself. So, you’ve pulled up Tri Merge credit report, using maybe smartcredit.com or PrivacyGuard or even myFICO. Okay. And what you notice is your credit scores are different. Experian is 760, Equifax 745, and in this example, ah, TransUnion 752. What gives? I’m the same person. Okay.

00:32 The scoring formula, let’s say it’s Fico 4, is exactly the same. So, why are they different?

00:37 Well, keep in mind, these are three different organizations, okay? But that doesn’t really affect the scoring formula because, as you know, it’s one scoring formula, especially if you’re on myfico.com. Okay. Um, so if all the data was exactly the same, you’d assume that the three credit scores were the same. But keep in mind your creditors, debt collectors, banks, lenders, they’re not, they’re not all necessarily sending the same data to all three credit agencies. So, you could have a bank that for whatever reason is only sending data to Equifax and TransUnion and for, for whatever reason, they’re not sending that same data to Experian.

01:20 Why they’re doing it? Um, various reasons. Is it common? No. Okay.

01:24 Also, what you’ll find is sometimes the bank or lender, um, they’ve updated Equifax and TransUnion for this month but they, their systems have, have not yet batched out that data to Experian yet. Okay.

01:35 So, you may have, ah, more positive, ah, reporting, more on-time payments reporting to Equifax and TransUnion on one particular trade line versus Experian. Okay.

01:46 Other more drastic cases that we see a lot more common were, were we’re seeing scores, you know, from 760 to 660 let’s say, um, are with collections. Okay.

01:55 So, let’s say you just incurred a collection. Okay. More than likely, that collection is gonna hit two out of the three credit agencies. It’s extremely common. Okay. The debt collector hasn’t, ah, subscribed to report to all three bureaus. Maybe just to save some bucks they’re only reporting to Equifax or they’re reporting to TransUnion and Equifax or just Experian. Okay.

02:15 So, this is gonna happen. And this is why when you go and get something like a home loan, the bank or lender, they’re never gonna use the highest score, they’re never gonna use the lowest score. Typically what they’re doing is they’re taking the median score. The median is the middle of three values. It’s not the middle of the page or the middle of your credit report, they’re usually using the middle of three values.

02:36 So, in this case if you went to get a mortgage, the bank or lender is usually gonna use your TransUnion credit score, if they are pulling a Tri Merge report. Okay.

02:44 Some other products, like car loans, they might only pull one bureau, they only subscribe to one bureau. But most things, like a home loan, the majority of our clients, you know, they’re always gonna use the median score for this reason, because they will vary.

02:58 Typical variations are somewhere within ten points. Okay. If the variations are more than that then that’s something you gotta dig into it. And when you look at that credit report, you have to analyze really, ah, negative marks. Have you had any negative marks and are they reporting to all three bureaus? Okay.

03:14 And one way you can figure that out is certain Tri Merge reports, reports that have all three bureaus, they will actually separate the data with Experian, Equifax and TransUnion. So, you can actually compare the three right on a credit report.

03:27 Now, if you’re looking at a, a credit report from a home lender, um, they’re usually using a Tri Merge where the data is actually merged. The payment history from all three bureaus will actually be all placed on one line. So you can’t actually see the difference between, ah, TransUnion, Ex-, Ex-, Experian and Equifax. Okay.

03:44 If that’s the case then what you can do is you can either subscribe to an online credit monitoring like myfico.com and actually separate that data.

03:51 Um, also you can ask your home lender to separate the data for you. So, your home, your home loan office should be able to call the company that they’re using to get their credit report. Some of those companies include, like, [inaudible 00:04:02] or LandSafe. And they can actually ask those companies, the company that put, mashed all the data together on their credit report, to separate the reports and actually submit them to see so you can see, if there is a drastic variation, what is the reason. Okay.

04:18 Also … Excuse me. Also, keep in mind, if there is a large variation, like, let’s say this 760, um, with Experian is now a 660 with, with Equifax. But we have the same actual accounts on the credit report. Right away, that’s a red flag that we have some sort of inaccuracy on the credit report. Okay. And that’s something that should be challenged.

04:39 So, if one credit agency is saying, “Hey, these payments are on time,” and the other agency is saying, “No, no, no, you have late payments,” well, we have an inaccuracy in some way, shape or form. And those late payments, if they are inaccurate, they need to get removed. So, that’s a pretty big red alert. Okay.

04:55 Um, guys, any questions regarding the difference between the three credit agencies, the variations of your credit score, by all means click below. There should be a Learn More button right below here if you’re on, ah, Facebook, and there should be a Click Here Sign Up for $0 Today button which should be kinda showing up right here.

05:13 This is Nik Tsoukales with Key Credit Repair, and this is your Credit Minute. Thanks.

Why did my Credit Score go Down when Nothing Changed?

Your Credit Minute Show Notes:

00:00 Hey what’s up guys, Nik Tsoukales from Key Credit Repair. We are gonna go through the credit question of the day, which is, why did my credit score drop even though nothing changed? Well, I have to tell you, something did change. Uh, just things you might not realize. So the credit report, keep in mind, is constantly changing. The credit score when you’re pulling it up online, or whether a lender is pulling it up, um, is going to pull data or it’s going to be a snapshot of the data in that moment. Now keep in mind from one moment to another things can change. Okay? And let me elaborate a little bit on that, ’cause some of the things you might think of haven’t changed, but I’ll actually break down some of the things that could have.

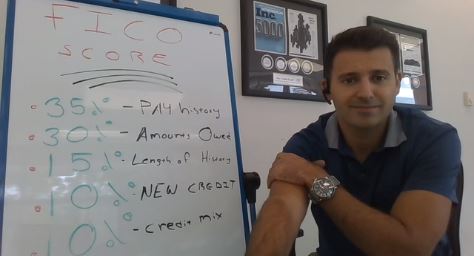

00:43 So, you’re going to notice here, I included a little chart here of what makes up your FICO score. Okay? So at 35 percent which is payment history, we 30 percent is amount owed or debt, 15 percent length of history, 10 percent new credit, and 10 percent credit mixed. So let me give you an example of some things that may have changed that you haven’t realized. Um, first thing is payment history. Okay? You might not have a new lay payment so you’re wondering, Nik why should my credit score change if I don’t have a new lay payment. Well maybe you’ve had a few more positive payments. That could actually cause your credit score to go up. Okay? Um, if you’ve had a recent lay payment obviously the credit score is going to go down. Okay?

01:27 Amounts owed. This is the big one. I would say this is the biggest culprit. Um, we get people that call us all the time and they will say my credit score has dropped five thousand points, five million points, I don’t know why. I haven’t been late, I haven’t done anything wrong. And in fact they really haven’t done anything wrong, but typically what we’re seeing is this part of the credit score is being affected because of something called, uh, credit card utilization rate. The proportion of your credit card balances compared to your credit limits affect this 30 percent of your credit score.

02:02 So let’s say, um, two months ago you pulled up your credit report and it was almost identical with the exception to the fact of, oh, with the exception to the fact that your credit card balance was 100 dollars. Okay? And when we pulled it up this time, the credit card balance was 300 dollars, and that credit limit is, is 500 dollars. Okay? Um, that utilization rate, okay, your proportion of balance compared to credit limit, um, is, has gone up considerably higher. Okay? And that will affect the 30 percent of what makes up your credit score. And obviously if, if that credit card utilization rate has dropped, this part of your credit score will benefit. Okay? So if you’ve pulled up your credit report recently or you’ve pulled up your credit score and there hasn’t been really any adverse change or new negative, uh, uh information, this is the first thing I would check out. Okay? It’s, it’s really the quickest opportunity to grab some points too. Okay?

03:03 Um, the next thing is, length of history. Okay, the length of history for your active accounts really affects your credit score in a pretty big way. It’s 15 percent of your credit score. So let’s say you have had a couple accounts that have just dropped off, some older accounts that were closed out a decade ago and they just fell off your credit report because of the statutes of limitations. Well that could adversely affect this part of your credit score as well. Okay?

03:28 The other thing is new credit. Let’s say if you’ve got a bunch of new, uh, credit cards recently, um, typically that will, you’ll see a small drop on your credit score. Okay? Um, probably if it just happened, you might see a quick 10 point drop in your credit score, but really over the course of 90, 120 days it should actually help your credit score pretty substantially because you’re gonna start getting on time payments on those cards. Which will positively affect the 35 percent of you credit score that’s payment history. Okay? If they’re credit cards, um, and you keep the balances at zero, it should help your credit score which is amounts owed. Um, because your credit card utilization rate, theoretically, should drop because your proportion of balance to limit has now dropped. Okay?

04:16 Um, and then we have credit mix. This is one no one is really talking about. Okay? Let’s actually circle this. The ideal mix is real estate number one. Uh, you have installment credit number two and revolving credit number three. Revolving being things like credit cards, lines of credit, overdraft protection. Installment credit is things like student loans, care loans, car leases, um, personal loans. Okay? And real estate credit being home equity lines of credit and mortgages. Okay? So let’s say your entire credit picture has stayed the same, um, but maybe you don’t have a car loan anymore. Maybe that balance was already down to like your last payment. The last time you checked your credit report recently was closed out. Um, this 10 percent of your credit score could be affected, ’cause you no longer have that perfect mix. You no longer have any installment credit. Um, maybe you have, uh, you know length of history maybe is gonna be a little more adversely affected if that auto loan was 10 years old and it just dropped off. Okay?

05:21 Um, so that could have an affect. Amounts owed really shouldn’t have an affect. Um, you could see an adverse affect from payment history, because now you have one less account reporting an on time payment. Okay? So there’s a little bit more than what’s, than what meets the eye with your credit score. There’s a lot that goes into it, but keep in mind the culprits typically are right here. Okay? The culprit is typically right here in amounts owed. So if you’ve seen your credit score drop or there’s been an adverse change, um, obviously if you’ve had a new late it would show up inside of payment history. If you haven’t and all of your accounts are intact, I want you to check your credit card utilization rate. Again, proportion of credit card balances to the available credit limits.

06:04 Guys this is Nik Tsoukales with your credit minute. Check us out at keycreditrepair.com for anything credit related. If you have any credit questions you’d like me to answer, uh, I’d be happy to, uh, drum out here on my fancy new little white board. And um, thanks for checking us out guys. Have a great day. Peace.

Protecting Your Child’s Credit Future

When it comes to credit scores and personal finances, there are several threats that people need to be aware of. There’s the actual financial aspect of credit issues, such as credit cards, debt, loans and more that need to be properly managed to maintain a good score. Then, there’s the aspect of identity theft, a serious issue that was highlighted last fall by the massive Equifax data breach, where about half of all Americans had their confidential information potentially swiped.

Yes, maintaining good credit is about a lot more these days than just forming good financial habits – and if you have children, part of your responsibility is raising them to learn from some of your generation’s mistakes. Among all the other responsibilities that you have as a parent, ensuring that your children have the knowledge to pave the way for a successful financial future is an important one. With that said, here’s a look at some ways you can help protect your child’s credit future, both from a monetary and identity theft standpoint:

Tips for Protecting Your Child’s Credit Future

Their name: Preventing identity theft arguably starts when you name your child. For instance, while it’s important for some families to follow tradition in naming their kids after their fathers or grandfathers, this can actually potentially implicate them when it comes to credit reporting. For instance, if David Jonathan Jones, Sr., has a negative item on his credit report, there’s a chance that David Jonathan Jones, Jr., may also have that same negative item on his credit report.

Beware of your online postings: Parents are proud of their kids, which makes sharing photos of them on Facebook, Twitter, Instagram and other social networks somewhat routine online behavior for them. That’s fine, but try to refrain from posting their birth dates, the city they were born in and other information a potential thieve could use to piece together information to steal their identity.

Freeze their credit: Experian estimates that about 25 percent of all children will have been victims of identity theft before they reach the age of 18. Noting this, consider calling up the credit bureaus and freezing your child’s credit. This ensures that nobody will be able to take out a line of credit in your child’s name unless they go through a rigorous process, which is very difficult for thieves to do. When it’s time to open a line of credit for your child, all you have to do is contact the bureaus and unfreeze it. To freeze their credit, you can go directly to the bureaus websites.

Discuss responsible money management: Certainly the other big aspect of ensuring a successful financial future for your child is instilling good money management habits. Start early in educating them on this important responsibility, and continue to speak with them about it as they get their first credit card, buy their first car and more. Irresponsibly managing money can lead to negative items on a credit report and significantly decrease their credit score, which can seriously jeopardize the things they’re able to accomplish in life.

The four aforementioned symptoms have all been linked to poor credit scores and credit card debt, according to consumer studies. In other words, bad credit can be bad for your health – and there’s some significant research to back this claim up.

Take a study recently published in the Proceedings of the National Academy of Sciences, for example. The study analyzed over 1,000 health records from birth to mid-life and found an alarming correlation between bad credit scores and heart health. Conversely, people with good credit scores were found to have had good heart health.

A separate study from Nerd Wallet discovered that more than 85 percent of surveyed Americans who have previously had or currently have credit card debt regret it. In citing reasons for regretting accumulating credit card debt, some of the answers weren’t surprising. Respondents stated reasons such as “it took too long to pay off” and “high interest rates cost me more money long term.” But there were a few other interesting reasons. For instance, stress and anxiety made the list.

Needless to say, but accumulating credit card debt can put you on the path to a poor credit score, which can thereby greatly impact your financial future. We don’t want to speak for all consumers, but that would certainly stress us out should we find ourselves unable to receive a reasonable auto loan or home mortgage.

The good news is that by enacting some credit repair strategies, you can boost your score rather significantly in a relatively short period of time. In the process, you can relieve some of that excess stress you’ve been carrying with you and possibly even improve your heart health. Here’s a closer look at some tips on how to do it:

How to Improve Your Credit Score

If you can’t pay off your credit card balance in full each month, you should at least be making the minimum payments. Ideally, however, you should be trying to keep your credit utilization ratio at or under 30 percent. The credit utilization ratio is essentially the amount of credit card debt you owe versus your total allotment. Your credit score should increase if it’s at or less than 30 percent.

Improve your consumer habits. If you’re in debt and can’t seem to get out of it, it’s likely time to take a closer look at your lifestyle. What things can you live without? Even the little things can add up long term and go a long way toward any debt management plan.

Don’t miss payments. We can’t stress this one enough, as it’s the single largest individual category that goes into calculating the FICO score. Miss a payment, and it could really cost you when it comes to your credit score.

So if you won’t take it from a financial expert to improve your credit score, perhaps you’ll take it from a doctor. After all, studies say it’s bad for your health. Doctor’s orders!

As a consumer, you should already know that a good credit score is a key cog to your financial future. But credit scores and credit reports can be complicated topics – and as is the case with most complicated subjects, misinformation is likely to spread. In this post, we’ve taken the liberty of debunking some of the most common credit score myths that we hear today. Have a look:

Myth 1: Making on-time bill payments is one way to help improve a credit score.

It’s important to make on-time bill payments, as it accounts for 35 percent – the single largest category – of the FICO score model. However, on-time payments won’t really help your score. Conversely, if you miss a payment, it can significantly hurt your score.

Myth 2: Closing unused credit cards will help improve a credit score.

This isn’t necessarily true – and for two reasons. First of all, credit history plays into your credit score, so closing an account may affect that. Secondly, closing an account can also affect your credit utilization ratio, or your debt-to-credit ratio. Generally, you want this to be 30 percent or less for the best possible score.

Myth 3: Checking your credit report will dock your score.

This is true, but only if it is a “hard pull.” Hard pulls are often performed by lenders during loan approval processes, and they may reduce your score by 10 points or so in the short term. Soft pulls don’t affect your credit score at all.

Myth 4: The more income you earn, the better credit score you’ll have.

That’s not true, as your credit score has no correlation to your earnings.

Myth 5: I only have one credit score.

That’s false. Though the FICO score is the most popular one, there are lots of different scoring models that lenders use.

Myth 6: Checking your credit report costs money.

While this can be true, it doesn‘t have to be true. That’s because by law, every American is entitled to one free credit report per year from the three major credit reporting bureaus (TransUnion, Equifax, Experian).

Myth 7: Credit reports offer fully accurate histories of consumer financial behavior.

Ideally, this is an accurate statement. However, it’s estimated that up to 20 percent of all Americans have some sort of error on their credit reports.

Myth 8: If there’s an error on my credit report, there’s nothing I can do about it.

The potential of an error on your credit report is part of why you should be checking it at least once a year. If you find one, you should immediately dispute it. Contact the credit bureau that issued the report to dispute the inaccuracy. It will be investigated and resolved within 45 days.

Myth 9: A large credit card balance won’t impact my credit score as long as I make the minimum payments.

That’s not true due to the credit utilization ratio that is taken into consideration. Generally, if this ratio is at or less than 30 percent, you’ll have a higher score than if it’s greater than 30 percent.

Myth 9: There’s no fast way to repair a credit score.

This may be true depending on the various factors that have led to a low score (i.e., bankruptcy, foreclosure, etc.), however, it’s important to keep in mind that credit scoring is fluid. Just paying down credit card balances to get within the 30 percent utilization ratio can yield a significant and speedy score increase in some cases.

Myth 10: If I have bad credit, it will be hard to get a loan.

There are opportunities to get loans no matter what your credit score is. However, being considered an at-risk consumer will unquestionably result in higher interest rates than if you had good or excellent credit.

What the Data Breach Prevention & Compensation Act Could Mean for You

The big Equifax hack of 2017 created a mess for a lot of American consumers. In fact, it’s estimated that about 143 million Americans were victimized in the hack, and the hack has the potential to be very detrimental in the long-term should the hackers take the confidential information that they swiped and put it to use. As if the hack wasn’t bad enough, Equifax was widely criticized for how it handled the matter and its lack of transparency with consumers. Bottom line: The hack was a raw deal, especially for American consumers. Equifax, while subject to bad publicity, might end up making money off of it in the long run.

There could be hope moving forward, however. A new bill introduced by U.S. Senators Elizabeth Warren (D-Massachusetts) and Mark Warner (D-Virginia) would penalize the credit reporting agencies in the event of any future data breaches. The thinking behind the bill is that any future data hacks wouldn’t just spell bad news for American consumers, but for the agencies that left consumer data susceptible too. The bill is a direct response to the perception that credit bureaus aren’t doing enough to protect the data they collect.

What this bill would mean:

There’s no word on whether the bill will be going to a vote, but here’s a closer look at what the bill would mean should it pass:

Credit reporting bureaus would be subject to regular inspection by the Federal Trade Commission (FTC) to ensure that they’re taking the proper measures to protect confidential consumer data.

Should a data breach occur, the FTC would be authorized to fine the credit reporting agencies $100 per consumer affected. The bill calls for half of the amount collected for such purposes to go to the consumers that were impacted. Think about that for a moment. If this bill were in effect when the Equifax hack occurred, the FTC could have collected up to $14.3 billion in penalties, with over $7 billion getting kicked back to the consumers who were victimized.

Senator Warren hasn’t been a stranger to proposing credit-related legislation. Following the 2017 Equifax hack, she proposed a pair of bills. One would have prohibited employers from making hiring decisions based on a person’s credit. The other would have allowed consumers to indefinitely freeze and unfreeze their credit any time they wished for free. Neither bill made it out of committee and to vote, however.

The Consumer Industry Data Association opposes the proposed bill, stating that the reporting bureaus already follow stringent enough standards. In a statement to CNET, its president and CEO said the bureaus would, however, like to work with Congress to make credit reporting safer and more secure.

The 2017 Equifax hack was blamed on a pair of issues – human error and a technical mishap. With that in mind, it’s enough to wonder if just one of the issues were to have been removed if the data breach would have occurred at all. For some, the proposed bill may be viewed as even more red tape in an already highly regulated field. But when it comes to data as confidential as social security numbers and credit information, can you really be too careful?

How the Holidays can affect your Credit Score

Tis the season…to be spending.

Yes, with the holidays fast approaching, chances are you’ve made your list (and checked it twice). But when it comes to holiday spending, you want to be sure that your credit score doesn’t get naughty, but stays nice. With all the spending you’re likely to do, combined with the increased threat of scammers this time of year, keeping your credit in good shape can be easier said than done. That’s why we’ve put together this handy list of tips and suggestions for how to prep for the holidays, while keeping your credit score in good shape. Here’s a look:

Tips and Suggestions for Holiday Spending (While Protecting Your Credit Score)

Use credit cards, not debit cards, to minimize impact of fraud: Any type of fraudulent purchase made on your credit or debit cards isn’t good, but those made on debit cards have the tendency to be a lot more impactful than those made on credit cards. That’s because the money spent can take more time for you to get back – and scammers are spending money that you already have in your account, not money that you’re promising to pay back later, as is the case with a credit card.

Be careful about where you shop: Another important tip to safeguard against scammers – be careful where you’re shopping, especially when it comes to online shopping! We get that things can get expensive around the holidays and you’re looking to save where you can, but be cautious about where you’re providing your credit card information. Look for the padlock symbol to verify site security, and if a deal seems too good to be true, know that it’s likely because it is too good to be true.

Watch your credit utilization ratio: We strongly suggest that you only charge purchases you know you can pay off before the end of the year, but regardless of your situation, it’s important to watch your credit utilization ratio, which is your debt versus your total credit allotment. Ideally, you want to keep this ratio at 30 percent or less for it not to lower your credit score. For example, if your credit limit on a card is $10,000, you want your spending to be $3,000 or less.

Refrain from opening new lines of credit: New credit cards don’t just have the potential to impact your credit utilization ratio, but every time you apply for one, your credit information is pulled, which also lowers your score.

Make on time payments: This accounts for 35 percent of your FICO score, so it’s incredibly important to make on time payments with any and all bills. Failure to do so will almost certainly lead to a significant drop in your credit score. In a perfect world, you should try carrying a zero balance on your credit cards and only charge what you know you can pay off each month. That’s not realistic for everyone, but regardless of the situation, making on time payments should always be a priority.

5 Fascinating Things You (Probably) Didn’t Know About Credit Scores

You’ve heard the old adage about how “knowledge is power,” and perhaps nothing demonstrates this saying more than when it comes to knowing about your credit information. Yes, the more you know about these details of your consumer history and you’re able to make better decisions when it comes to your future behavior.

First and foremost, it’s important to know your credit score, but it’s never a bad idea to brush up on some of the more intricate details that shape your score.

Here’s a look at five things you probably didn’t know about credit scores:

5 Interesting Credit Score Facts

The big 5: Do you know the five factors that go into calculating your credit score? You should! Payment history is the largest single factor, worth 35 percent of your score. It validates the importance of paying your bills on time. Credit utilization ratio is next, at 30 percent. For a good lender-friendly ratio, keep it at 30 percent or less. Length of credit history factors into 15 percent of the score, and new credit and your credit mix each account for 10 percent of the score.

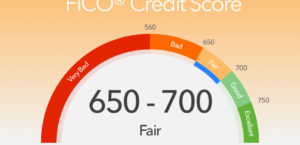

700: That’s the credit score of the average U.S. adult. A score of 700 is considered to be in the “good” category. This “good” category applies to scores between 670 and 739.

Do you know your score? If you don’t know your score, you aren’t alone. In fact, it’s estimated that three out of every five Americans don’t know what their credit score is. That’s 60 percent of the country, and there’s really no excuse for it based on how important that three-digit number is to your purchasing power and how easy it has become to access.

Credit report doesn’t equal credit score: Up to 20 percent of all credit reports contain some sort of error. That’s why it’s a good idea to utilize your right to obtain a free annual credit report. But contrary to what many believe, checking your credit report doesn’t permit you access to your actual credit score. We know it seems odd, but that’s the way it works. To get your score, check your credit card statements, subscribe to a free credit check website or talk to your bank or credit union.

Late payments can do terrible things to your score: As we noted above, payment history is the largest consideration factor when it comes to calculating a credit score. Noting this, it probably doesn’t surprise you that late or skipped payments don’t bode well for your score. But what you may be surprised to learn is just how hurtful they can be. In fact, a 30-day late payment could cause your credit score to dip an entire 100 points! The lesson: Pay your bills on time!

FICO Credit Score? A crucial aspect of knowing whether or not you’re in need of credit repair is obviously learning what your actual credit score is. After all, those crucial three digits are what lenders look at when deciding how at-risk of a consumer you are and whether or not your application should be approved or denied on everything from mortgage loans to auto loans to student loans. But how consumers attain this credit score information is a topic that has always been up for debate.

The aspect of how to attain credit scores recently made headlines again, as two of the leading credit reporting agencies in the United States were fined for allegedly charging consumers to check their credit scores – a practice viewed as unethical and misleading by the Consumer Financial Protection Bureau. In light of these recent events, the question remains: Should consumers pay for their FICO scores? Or should they rely on free avenues for attaining this crucial data?

FICO Credit Score. Where to Get Free?

Most experts advise consumers to check their credit scores and credit reports at least once a year. This is suggested even for consumers with very good credit, as checking such information annually can help detect potential errors and lead to quicker all-around fixes. Federal law permits consumers to attain credit reports free of charge from the three main credit reporting agencies once a year. Consumers that are looking to repair credit to make themselves more attractive on a loan or credit card application, however, may need to check their scores more frequently than annually to judge where they stand. The good news is that more and more outlets are making it easier to do this on a complimentary basis.

Here’s a look at some of these free avenues available for checking your FICO Credit Score:

Your bank or credit union: Many financial institutions will offer free credit score checks for members. Some may even offer complimentary consulting services to help consumers reach their credit score goals.

Your credit card company: Credit card companies like Discover now offer free credit scores to both cardholders and non-cardholders. Citi and Chase have similar policies. Others may provide your credit score if you simply ask.

Websites: If you go the route of getting your credit score through a website, it’s important to make sure that the site is a credible one (i.e. CreditKarma) and that you aren’t supplying your credit card information for the service. Credible credit reporting websites will help provide you regular credit score updates, as well as provide guidance on potential purchases based on your score.

Applications: Applying for a new credit card, car loan, or refinancing? As part of the approval process, the lender will be surely checking your credit score to make sure you qualify. Take advantage of this situation to learn what your credit score is.

We should note that you can buy your credit score. However, you should only ever consider doing so when you’ve either exhausted the options that we’ve listed above or if none of the aforementioned complimentary means of acquisition are viable for FICO Credit Score.

Black Boxes That Are Credit Scores

The concept of a Black Boxes is actually derived from the science and engineering fields. Specifically, Black Boxes are defined as something that you can view externally, but have no understanding of how it works internally. The same concept can be applied to credit scores, as many consumers just take note of the three-digit score that they get, yet have no idea of how – and why – it is what it is.

A Google search will quickly provide you with how the FICO score is calculated, but consumer beware – there’s also a lot of misinformation about credit scores and scoring formulas on the Internet as well. You could say that the formula itself behind the credit score isn’t that big of a mystery. The mystery is how that formula is navigated and what parts of it are stressed by the consumer. This post is designed to help you better debunk the black boxes when it comes to credit scores.

Black Boxes that are Credit Scores In a Nutshell

As you likely know, your credit score is essential to getting approved for a mortgage, auto loan, student loan and more. But what you might not know is that there’s more than just one credit score. In fact, while the FICO score is the most popular, there are dozens of credit scores that lenders may choose from based on the data that is reported to the three major credit bureaus. Because of the various different credit scores, and the fact that new formulas are always coming out, this confuses people. It’s why we encourage consumers to pull their credit report at least once a year and pay more attention to the data – not necessarily the three digit number that they get. Understanding the data is what’s really important when it comes to determining whether or not you have good credit – and how you can improve your credit score.

A Credit Repair Plan

Say you want to buy a home, but your credit isn’t good enough to get approved for a mortgage. Or maybe you want to further elevate your credit score so you can lock in a lower interest rate. That’s where a credit repair plan is necessary, as you need to know what your current score is and how much you need to elevate it to meet your goal. This is the point where the “3 Ups” come into play:

Clean Up

Build Up

Pay Up

Before you can truly put a credit repair plan into place, you need to know why your score is what it is, and make a plan to clean it up accordingly. After this, you need to analyze ways that will allow you to build your credit back up. And then, finally, there’s likely to be debts that you have to pay off in order to get your debt-to-credit ratio to at or below 30 percent to really notice an improvement on your score.