Pop quiz: What happens to your debt after you die?

A) If you have a co-signer on your mortgage or credit cards, debt collectors will come after him/her for finance payments.

B) Your estate will pay off the remainder of your debt.

C) Certain debt is passed on in your will.

D) Creditors have to eat remaining debt.

Depending on your situation, all of the above may be true, whether you’re dealing with medical debt, mortgage payments or credit card debt. That’s because there are a lot of different scenarios that can play out depending on what arrangements a certain person has made – or didn’t make – when they were still alive.

Hypothetically speaking, say your spouse of 50 years passed away suddenly. You co-signed with your significant other on a home loan, which is paid off, and on a credit card, which has a $3,000 balance on it. Because you co-signed on the credit card, you’re responsible for paying it off. Failure to do so will be reflected in your credit history and credit report.

But say, for instance, that your 85-year-old mother passed away, leaving behind medical debt. Her estate would be responsible for settling this debt and then everything left over would go to her heirs. So, for example, the valuables your mother accrued over her lifetime – car, home, etc. – would be used to settle any outstanding debt. If there isn’t enough money to pay debt off, then her estate is declared “insolvent” and her creditors would have to eat the outstanding debt. So here’s a credit tip – if an estate is declared “insolvent,” heirs don’t have to worry about how any outstanding debt will impact them, meaning that no lengthy credit repair measures need to be enacted on anyone’s behalf – even if aggressive debt collectors still come knocking.

In some cases, however, someone may pass along a home with a balance on it to a loved one in their will. If that’s the case, this loved one is the new owner and can either decide to enact a debt management strategy to finance the remainder of the home or they could sell it and pay the remaining balance off with what it is purchased for.

For additional information on how to repair your credit, please Sign Up for $0 Today.

Fix your credit – Get approved for a loan!

In today’s world, credit scores are more important than ever. Without a good credit score, it’s virtually impossible to attain a house, car or anything that requires long-term repayment. The good news is, while a good credit score is crucial, a bad score can get fixed more quickly than you might think. Here are some good credit tips for shaping up your credit score as you prepare to purchase a house.

The Big Picture

Before you can repair credit, you have to understand exactly what you’re repairing. For most people, this means fixing a spotty payment history and a high debt-to-credit-limit ratio. These two factors comprise 65 percent of your FICO score, with payment history being a slightly more important factor.

Credit Report Review

Your first step in the credit repair process is pulling your credit report and looking for errors. An estimated 80 percent of credit reports have errors, and a quarter of these errors can impact your ability to get a loan. It’s important to take note of any inaccurate information, particularly late payments that weren’t truly late. Disputing these errors and getting them removed will improve your credit score significantly.

Reducing Debt

When applying for a mortgage, the bank wants to assess your debt management skills. Carrying large credit card balances isn’t the way to show that you’re a responsible money manager. Get your balances as low as possible before beginning the mortgage application process. You’ll want to have card balances no higher than 30 percent of your credit limits.

Managing Inquiries

Every time you apply for credit, an inquiry is noted on your credit report. This normally isn’t a big deal, and counts for just 10 percent of your FICO score. That said, too many inquiries in a short period of time makes you look like you’re desperate for cash, and it might turn a bank off from lending to you. Make sure you have as few inquiries as possible as you prepare to buy a home.

Why Credit Scores Matter

You might be able to get a mortgage with a credit score of 660, but you won’t get as good a rate as someone with a score of 740. That difference could add up to thousands of dollars in finance charges over the life of the mortgage. It’s in your best interest to get your credit score in the best shape possible before you apply for a mortgage. The higher the score, the less you’ll end up paying for the house of your dreams. For additional information on how to repair your credit, please Sign Up for $0 Today.

Getting Preapproved for a Car Loan – Saving You Money, Time & Hassle!

A traditional part of the home buying process is also part of the best vehicle shopping experience. The process of obtaining preapproval for an auto loan is now catching on as smart car shoppers realize the savings and control it can offer them. If are preparing to shop for a car and plan to finance the purchase, here are some credit tips and helpful information to get you started.

How to Prepare for the Application Process

Similar to the home loan process, getting preapproved for an auto loan starts with your credit score. Lenders want

to see proof of your debt management skills in the past, before offering you a loan.

It is very important to take time to make sure that your credit report is accurate, before you apply for preapproval

of any loan. Even small errors can mean higher interest rates or the embarrassment and disappointment of being denied

for the car loan, so take the time to make sure all information is correct. It is always best to repair credit, if needed,

prior to the application process.

If you find an inaccuracy on your credit report, taking the time to correct these will greatly improve the preapproval

process and your chances of getting a great rate on the loan, itself. If you have blemishes on your credit that will influence

your borrowing status, it may be wise to seek reputable credit repair assistance, before proceeding.

Making Application

After you are satisfied that your credit report depicts a fair, and honest, portrait of your borrowing and repayment history, now you are ready to begin contacting lenders and begin the application process. This should be done before you begin looking at vehicles, so that you will know exactly how much you want to spend, and you will be better able to resist the temptation to splurge on a car that is more expensive than what you need.

As you speak with the lender, verify any restrictions that they may place on the loan. Lenders may restrict purchasers of new vehicles to shop at established dealerships. Restrictions for a pre-owned vehicle often include restrictions on the age, type, condition and mileage of the vehicle you are considering. This is done to ensure that the vehicle’s value will support the amount of the loan, in case you default and leave the lender to sell the car.

Time To Shop

Once you have found the auto loan that best fits your needs and obtained preapproval, it is time to shop. Keeping in mind any lender restrictions and your preapproval limit will help you set parameters for your search that will make it easier to quickly locate a great vehicle.

When you have found the right vehicle, your preapproved loan status can often be used as a negotiation tool, sometimes resulting in a better offer from the dealership’s finance department.

For more information on how to repair your credit prior to getting preappproved for an auto loan, Sign Up for $0 Today.

Credit Cards of the Future – Credit News

Credit cards have been used for over 60 years. Back in the 1950s, they completely revolutionized the way transactions took place, and the ease with which we could access our cash. Unfortunately, technology and the world have changed a lot since the 1950s, while credit card technology has barely advanced. This has resulted in an increasing number of security issues related to credit card fraud,

which is costing consumers and businesses billions of dollars every year. Fraudulent charges have forced consumers, through no fault of their own, to deal with debt management, credit repair, and other finance services to recover their credit score.

Technologies that will change the way credit cards are used

In response to these problems, a number of new technologies are on the horizon that will eventually be incorporated into credit cards throughout the United States. One of the most promising technologies is microchips embedded into each card. Microchips are much more secure than magnetic strips, and are already being used in Canada and Europe. Another promising series of technologies are offered by Dynamics, and include the cards that can hide a portion of the credit card number until it is needed and cards that can be linked to more than one account. Fewer cards means fewer accounts to keep track of, and these technologies promise to dramatically reduce the number of consumers who need to repair credit after someone tries to hack their accounts.

Why new credit card technologies have been delayed

While some might look at these new technologies and think that the most obvious credit tip would be to get a card with them integrated, the reality is not so simple. Many of these technologies are not yet available for the mass market. While Canada and countries in Europe have largely adopted microchipping, the United States has resisted for a number of reasons.

Perhaps most significantly, there has been a lot of resistance from businesses, which will be required to purchase all new merchant processing equipment, including back office equipment and cash registers. With the economy still fairly weak, asking businesses to take on additional expenses is a tough sell for legislators. Moreover, the value of the microchipping and other technologies are largely useless if they are not widespread and able to be utilized everyone traditional credit cards are.

However, with billions of dollars in credit card fraud every year, hopefully the tides will soon change, and we will be able to secure our personal assets with the credit cards of the future.

Bad Credit Aftermath – How Much it Can Cost You?

How Much Does A Bad Score Really Cost You?

Common sense will tell you that having a good credit score is much better than having a poor credit score, as far as loan approval and interest rates go. But do you really know how much a bad score can really cost you? You might be surprised.

Take a 30-year mortgage for example. Now take a good credit score (680-699), an excellent credit score (740+) and a poor credit score (620-639). Here’s a look at the breakdown of possible costs over the course of a hypothetical $200,000 home loan:

Excellent credit (4.025 percent): A likely monthly payment of $958, which equates to an $11,493 annual cost and a $344,798 lifetime cost.

Good credit (4.974 percent): A monthly cost of $1,070, annual cost of $12,846 and lifetime cost of $385,368.

Poor credit (5.418 percent): A monthly cost of $1,133, annual cost of $13,598 and lifetime cost of $407,950.

As you can see, having an excellent credit score can save you up to $113 per month and $40,591 over just having a “good” credit score over the course of a 30-year mortgage. And an excellent score can save you $175 per month and $63,173 over a “poor” credit score. Hence, taking measures to repair credit before financing such a significant purchase is crucial to your short- and long-term finances.

So just what are some credit tips to repair a poor score?

On-time payments

Keeping debt within 30 percent of your total credit allotment

Having a diversity of different credit

Having a lengthy credit history

As if having a favorable credit score wasn’t important enough, the above examples certainly place even more significance on the importance of credit repair and debt management if you’re in a financial bind. As the above examples show, a good credit score could mean the difference of tens of thousands of dollars over the course of a long-term loan. That’s a lot of money that you surely could put toward other purchases and a big incentive to take measures to improve your credit score today.

Making on-time payments, enacting a debt management strategy so that you don’t owe more than 30 percent of your total credit limit, and having a variety of different types of credit are all things that you can do to ensure a good, healthy credit score. But one common credit score killer is medical bills – and many times, your score could suffer due to a misunderstanding with your insurance or your doctor, potentially docking you big points for something that isn’t necessarily your fault. Other times, your score could suffer because you simply just can’t afford the cost.

In fact, medical bills that go to collections are treated the same way as any other type of bill that goes to collections in the FICO score formula. Analysts say that just one medical bill that has gone to collections could drop your credit score by 100 points, thereby forcing you to enact a lengthy credit repair strategy to bring the score back up over time.

So what can you do to ensure that a bill doesn’t go to collections? Here’s a look at some credit tips:

Understand your insurance: Many medical bills go to collections because people can’t afford to pay them. One way to better plan and prepare for potential medical costs is to know and understand your insurance plan. For instance, does it cover wellness visits? What’s the deductible? Will you have to pay money out-of-pocket after you meet the deductible? Knowing all these things can better help you prepare in the event of a surgical procedure or emergency rather than take a “wait and see” approach for when the bill arrives.

Go on a payment plan: Surgeries, procedures and hospital stays can all add up. And many people can’t afford to pay the total bill in full right away. Check with the hospital to see if you can go on a payment plan to make regular installments toward the bill. Many hospitals won’t charge any interest as long as the balance is paid within a year or two. Others may allow you to finance bills.

Keep records: Be sure to retain all your medical bills and check your credit report regularly to watch for inaccuracies. It’s estimated that four out of every five credit reports have errors in them, so if your report doesn’t line up with your personal records, take action to have any discrepancies removed from your report. Otherwise, you could have to repair credit for nothing.

While credit scores and credit reports are most commonly associated with loan approvals, there’s more than just getting approved for a credit card, auto loan or mortgage that the little three-digit FICO score is used to calculate.

For instance, credit scores are also factored into things like auto insurance premiums. Yes, credit scores count for insurance too, which makes credit repair all the more important and quite the lesser known credit tip.

So just how is a credit score factored into an insurance premium? An insurance provider will typically base premium rates on an insurance score. And this insurance score takes into account your credit history in order to predict your likelihood of being involved in an accident or filing an insurance claim. Studies detail how credit history can be linked to risk and accident potential.

Here’s a closer look at a credit-based insurance score and why it’s important that you repair credit for more than just good interest rates on loans:

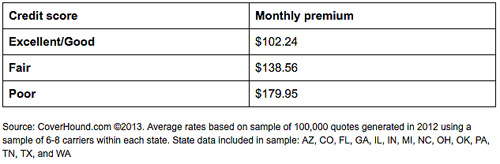

The higher your credit score – and thereby your credit-based insurance score – the greater the likelihood that you’ll qualify for low auto insurance premiums. Keep in mind that this premium also takes into consideration driving history and the amount of claims on your record.

If you have a low credit score, you’re more likely to pay more for your auto insurance premium, as you’ll likely have a lower overall credit-based insurance score.

If you have less than stellar credit, what can you do to improve it for auto insurance purposes? The same thing you would do to improve it for any other purpose:

Make sure payments are on time.

Open new credit lines in good standing.

Have a favorable credit history (i.e., no collections, missed payments, etc.)

Good debt management – try not to accrue more than 30 percent of your total credit line at once.

Yes, good credit is about more than just low interest rates on loans – it can also net you lower auto insurance premiums. So if your credit is lacking, take measures to get your finances in order today.

Credit After Divorce – Managing Things After This Hard Time

When you get divorced, the person you thought was “the one” might not be the only thing you lose – your credit score could also suffer! Yes, financial problems have the potential to crop up during a divorce, especially if you’ve co-signed loans with your soon-to-be ex. Divorces can be messy enough, but yes, they can take a toll on your credit too!

With that being said, here’s a look at some ways to manage your FICO score through divorce, so you’re not stuck in a lengthy credit repair plan later:

Close or refinance all shared accounts: During a split, courts will divide shared debt through what’s called a divorce decree. But what the courts and lawyers won’t tell you is that these decrees don’t eliminate shared responsibility. For instance, if your ex is tasked with paying the auto loan and misses a payment – the late payment will show up late on your credit report too, hurting your score and staying with you for years! So along the lines of a credit tip, don’t take any chances and refinance any loans that were previously shared if you’re able to.

Cooperate with your ex: While you’re divorcing for one reason, it’s important to work with your ex on your finances for the sake of not having to repair credit down the line. Hence, along the lines of our first bullet point – not every loan can be refinanced quickly. So for loans that can’t, be sure that you strike a truce with your ex to ensure that payments are made. If they’re not they hurt both of your credit scores. Online accounts and automatic payments are ways to make this easier.

Credit monitoring: Divorces can get messy, and there’s no telling what your ex might do to your credit score as a means of revenge if they know of your social security number and financial details. That’s why signing on to a credit monitoring service is a good idea – it’ll immediately make you aware of any changes to your credit data, potentially permitting you to avoid implementing a big debt management plan later for the damages incurred.

Paid Collections – Why Are They Still on My Report?

Are you one of many Americans who have collection accounts on your credit report? If so, you unquestionably want it to just go away. This is a pivotal part of credit repair but raising your credit score back up to a favorable status is much easier said than done. That’s because according to U.S. law, collection accounts can be reported in your credit history for seven-and-a-half years from the original date you fall behind on payments.

Yikes!

Seven-and-a-half years. That’s a long time a bad record can weigh down your FICO score. Even worse, it’s possible that you can settle your debt with a collection agency and the record will still weigh down your credit score. Why? Because collection agencies are required to report information that is both accurate and complete and that includes this negative aspect of your credit history.

So now that you know why collection agencies won’t wipe a record clean, even after you’ve settled your debt, you might be wondering if there’s anything you can do? I mean, 7.5 years is a long time to wait out a bad record.

The good news is that there are some things you can do to wipe bad records from your report early, thereby allowing you to advance and repair credit. The bad news is these things are not sure-fire. Here’s a look at a few credit tips for working with collection agencies on this matter:

First, pull your credit history so you know what’s being reported. There’s a chance you might find an inaccuracy within the report, which can lead to a favorable outcome, as collection agencies aren’t legally allowed to report inaccurate or incomplete information.

Negotiate a “pay for removal” debt management deal: If you haven’t settled any debt yet, contact the collection agency and see if they will remove your record should you settle the debt. Many will likely respond and say that they’re unable to remove the record, as credit reporting agencies frown upon this policy. But it’s worth a shot.

Build new, positive credit: Part of your credit score is based on any new credit you’re building. So if you’re striking out with getting records removed from your credit report, it may just be best to cut your losses and focus on building new credit. As time goes on, these negative records will have less of an impact on your overall score, as long as your finances and credit history are headed in the right direction.

For more information on how to repair your credit after a collection you can Sign Up for $0 Today.

Bad Credit Score – It Hurts!

Everyone knows that a good credit score is essential to getting approval for everything from car insurance to car loans—and for getting the best possible interest rate that’s currently being offered—but what many people don’t seem to realize is just how much of a toll a poor FICO score can have on you.

So if you have a poor score, it’s important to take it seriously and enact credit repair, whether it means deploying debt management techniques or implementing good bill-paying habits. Here’s a look at how a poor credit score can hurt you and your finances.

High credit card interest rates: Credit cards are notorious for the high interest rates they charge. After all, it is how the card companies make their money. However, if you have poor credit, you can anticipate paying 22 percent and upward, should you even be approved. That’s a far cry from the 10 to 19 percent that’s likely with a good score.

Loan interest: How much more can you expect to pay on a car loan with a poor credit score? Possibly up to 2 whole percentage points of interest! Mortgage loans, too, can mean you that you will have to pay potentially tens of thousands more over the course of a loan with a poor score. Repair credit, and take it seriously to avoid these preventable expenses.

Miscellaneous: Can you imaging trying to sign up for a cell phone plan only to find out at the store that you’re ineligible because your credit score isn’t good enough? It happens. The same goes with car insurance. Presently, 47 states are permitted to check your credit score to determine the rate.

As you can see, a poor credit score can really hurt! So if yours isn’t satisfactory, make sure you’re taking the proper steps to correct it.

More Insurance Tips

Understanding General Insurance coverage: Suggestion For The Smart Consumer

When it comes to dealing with insurance coverage, it may seem like it is you versus the globe in some cases. With the huge quantity of information available online, it can be almost overwhelming at. This article will certainly offer much practical info for you to obtain begun on the appropriate course.

When you make any sort of improvements to your house that price over a specific amount, you should make sure to call your insurance company and allow them find out about it. If requirement be, many insurance carriers make you state renovations to them that cost a lot so that your plan can be readjusted.

Keep your broker or insurance firm updated on anything that may affect your policy or protection. If they do, then they could propose the next program of activity in concerns to your insurance coverage plan.

When you decide on insurance coverage for your auto, certify your insurer. Evaluating protection, it is additionally in your best passion to look for evaluations on their client solution, case responsiveness and also also rate increases. Understanding which you are dealing with ahead of time can aid you set assumptions with your insurance firm.

Commonly, you will want to get in touch with other client testimonials of specific insurance policy business just before spending your cash in their policies. By speaking with sites like Angie’s listing as well as other such customer remarks, you can acquire a sense of the current popular opinion towards an insurance policy business. If the majority of the firm’s patrons are pleased, that may aid you develop a choice, and also vice-versa.

Have your insurance coverage company reconsiders your scores if your credit history rating has gone up. Insurance business do base component of your preliminary premium on your credit report. Without your consent though, they could just inspect it when they initially supply you protection unless you have had a lapse of insurance coverage. If you know your credit has risen, having your credit rating reconsidered could possibly bag you a reduction in your costs.

When comparing insurance business, the wise customer will certainly take their own loyalty right into account. An insurer that has supplied years of reliable, hassle-free and also reputable service need to not be deserted the instant a slightly more affordable different becomes available. It is fairly most likely that an insurance firm that provides rock-bottom prices is cutting corners somewhere in the solution they provide their clients.

An annual review of their insurance plan is a routine every person ought to exercise. Make certain that all details on your plan is correct and also update it with any type of adjustments. See to it you are receiving credit report for such points as automated seat belts on your automobile policy and safety surveillance on your property owner policy.

In summary, you would like to do all that you can to learn concerning insurance policy. There is a lot of information available, yet we have given a few of the most essential pointers. Ideally we have supplied you with sufficient details to not only provide you a strong background, however additionally further spark your passion to come to be a professional in it.

If they do, then they could recommend the following course of action in regards to your insurance policy. Typically, you will certainly want to speak with other consumer assessments of certain insurance coverage companies just before investing your cash in their plans. If your credit history rating has gone up, have your insurance provider company rechecks your ratings. Insurance policy firms do base part of your initial premium on your credit rating rating. An annual testimonial of their insurance policies is a routine every person need to engage in.