Why did my Credit Score go Down when Nothing Changed?

Your Credit Minute Show Notes:

00:00 Hey what’s up guys, Nik Tsoukales from Key Credit Repair. We are gonna go through the credit question of the day, which is, why did my credit score drop even though nothing changed? Well, I have to tell you, something did change. Uh, just things you might not realize. So the credit report, keep in mind, is constantly changing. The credit score when you’re pulling it up online, or whether a lender is pulling it up, um, is going to pull data or it’s going to be a snapshot of the data in that moment. Now keep in mind from one moment to another things can change. Okay? And let me elaborate a little bit on that, ’cause some of the things you might think of haven’t changed, but I’ll actually break down some of the things that could have.

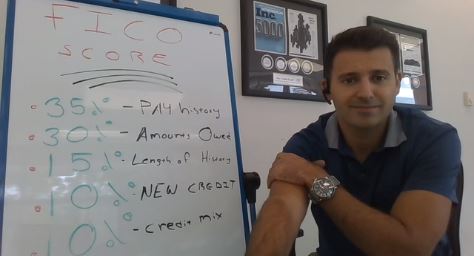

00:43 So, you’re going to notice here, I included a little chart here of what makes up your FICO score. Okay? So at 35 percent which is payment history, we 30 percent is amount owed or debt, 15 percent length of history, 10 percent new credit, and 10 percent credit mixed. So let me give you an example of some things that may have changed that you haven’t realized. Um, first thing is payment history. Okay? You might not have a new lay payment so you’re wondering, Nik why should my credit score change if I don’t have a new lay payment. Well maybe you’ve had a few more positive payments. That could actually cause your credit score to go up. Okay? Um, if you’ve had a recent lay payment obviously the credit score is going to go down. Okay?

01:27 Amounts owed. This is the big one. I would say this is the biggest culprit. Um, we get people that call us all the time and they will say my credit score has dropped five thousand points, five million points, I don’t know why. I haven’t been late, I haven’t done anything wrong. And in fact they really haven’t done anything wrong, but typically what we’re seeing is this part of the credit score is being affected because of something called, uh, credit card utilization rate. The proportion of your credit card balances compared to your credit limits affect this 30 percent of your credit score.

02:02 So let’s say, um, two months ago you pulled up your credit report and it was almost identical with the exception to the fact of, oh, with the exception to the fact that your credit card balance was 100 dollars. Okay? And when we pulled it up this time, the credit card balance was 300 dollars, and that credit limit is, is 500 dollars. Okay? Um, that utilization rate, okay, your proportion of balance compared to credit limit, um, is, has gone up considerably higher. Okay? And that will affect the 30 percent of what makes up your credit score. And obviously if, if that credit card utilization rate has dropped, this part of your credit score will benefit. Okay? So if you’ve pulled up your credit report recently or you’ve pulled up your credit score and there hasn’t been really any adverse change or new negative, uh, uh information, this is the first thing I would check out. Okay? It’s, it’s really the quickest opportunity to grab some points too. Okay?

03:03 Um, the next thing is, length of history. Okay, the length of history for your active accounts really affects your credit score in a pretty big way. It’s 15 percent of your credit score. So let’s say you have had a couple accounts that have just dropped off, some older accounts that were closed out a decade ago and they just fell off your credit report because of the statutes of limitations. Well that could adversely affect this part of your credit score as well. Okay?

03:28 The other thing is new credit. Let’s say if you’ve got a bunch of new, uh, credit cards recently, um, typically that will, you’ll see a small drop on your credit score. Okay? Um, probably if it just happened, you might see a quick 10 point drop in your credit score, but really over the course of 90, 120 days it should actually help your credit score pretty substantially because you’re gonna start getting on time payments on those cards. Which will positively affect the 35 percent of you credit score that’s payment history. Okay? If they’re credit cards, um, and you keep the balances at zero, it should help your credit score which is amounts owed. Um, because your credit card utilization rate, theoretically, should drop because your proportion of balance to limit has now dropped. Okay?

04:16 Um, and then we have credit mix. This is one no one is really talking about. Okay? Let’s actually circle this. The ideal mix is real estate number one. Uh, you have installment credit number two and revolving credit number three. Revolving being things like credit cards, lines of credit, overdraft protection. Installment credit is things like student loans, care loans, car leases, um, personal loans. Okay? And real estate credit being home equity lines of credit and mortgages. Okay? So let’s say your entire credit picture has stayed the same, um, but maybe you don’t have a car loan anymore. Maybe that balance was already down to like your last payment. The last time you checked your credit report recently was closed out. Um, this 10 percent of your credit score could be affected, ’cause you no longer have that perfect mix. You no longer have any installment credit. Um, maybe you have, uh, you know length of history maybe is gonna be a little more adversely affected if that auto loan was 10 years old and it just dropped off. Okay?

05:21 Um, so that could have an affect. Amounts owed really shouldn’t have an affect. Um, you could see an adverse affect from payment history, because now you have one less account reporting an on time payment. Okay? So there’s a little bit more than what’s, than what meets the eye with your credit score. There’s a lot that goes into it, but keep in mind the culprits typically are right here. Okay? The culprit is typically right here in amounts owed. So if you’ve seen your credit score drop or there’s been an adverse change, um, obviously if you’ve had a new late it would show up inside of payment history. If you haven’t and all of your accounts are intact, I want you to check your credit card utilization rate. Again, proportion of credit card balances to the available credit limits.

06:04 Guys this is Nik Tsoukales with your credit minute. Check us out at keycreditrepair.com for anything credit related. If you have any credit questions you’d like me to answer, uh, I’d be happy to, uh, drum out here on my fancy new little white board. And um, thanks for checking us out guys. Have a great day. Peace.

If you’re a military member with security clearance, you may be aware of a recent change that the Department of Defense (DoD) is now enforcing. Specifically, the DoD has been instructed by the president to “continuously” monitor personnel with security clearance. While this “monitoring” encompasses several different things, one important aspect of this new policy that military members should be taking stock of now is their financial history. Yes, the DoD will be regularly monitoring the likes of credit scores and credit reports for any warning signs that could draw concern. So if you’re a military member that has access to classified information, it’s time to brush up on your credit report, aim to lower your debt-to-credit ratio and commit to better meeting your financial obligations (if you don’t already do so). Failure to do so, and you could lose your access and potentially derail your career.

This post will take a closer look at the steps military members with security clearance should take to ensure that they are in good credit and financial standing.

Steps to Make Sure Your Credit Doesn’t Affect Your Clearance

Keeping tabs on your credit, and enacting good debt management and credit repair practices is something that consists of the same general tactics universally, whether you have special security clearance or are just an average civilian. Here’s a look at what you should be doing:

Check your report: Here’s something that everyone should know: You’re entitled to one free credit report annually from each of the major credit bureaus. It’s important to make sure that you’re taking advantage of this for several reasons. One, it gives you a good idea of where you stand and what work you need to do. Two, it can help you detect and dispute any errors that are on your report. The latter point is especially significant, especially when you consider that as many as one-fifth of all Americans have some sort of error on their credit report. So even if you’re in good credit standing, make sure you pull your report to see if there are any inconsistencies.

Sign up for fraud alerts: One nice thing about the new guidelines that will require continuous monitoring of personnel with security clearance is that as of May 2019, service members will be able to enroll in complimentary credit monitoring and fraud detection. Until this new policy takes place, however, service members might consider contacting the credit reporting bureaus and ask them to freeze their credit. Freezing credit essentially means that nobody will be able to open a line of credit under your name until you un-freeze it. It provides an extra layer of security and peace of mind.

Commit to good debt management, credit practices: As we stated in the opening, anything that raises eyebrows during the DoD’s continuous monitoring has the potential to be detrimental for active service members. That said, if you haven’t already done so, now’s the time to commit to good debt management and credit score practices. Make sure that your bills are paid on time, try to keep your debt-to-credit ratio at or under 30 percent, wisely open and close new and existing accounts, respectively, and make sure that you’re regularly checking your credit score and annually pulling your credit report.

While some active service members with classified access might think of the new regulations as a bad thing, we encourage you to look at it as a way of getting that kick in the butt to make sure that you’re in good credit standing. And if you’re not, there’s no time

How to Save for Your Child’s College Without Breaking Your Own Bank

Here’s the understatement of the century: College is not cheap. In fact, the average tuition cost for in-state students at public universities is currently about $10,000 a year. And that doesn’t include room and board, meals or books.

Like we said, college isn’t cheap – and that’s why it behooves parents to begin saving for it as soon as possible. So how can you start saving for your child’s college education without having to live off ramen noodles and cheap beer yourself? Here’s a look at some tips and suggestions:

How to Save for Your Child’s College Education

529 Plans: 529 plans are available in every U.S. state and are purpose-designed to help parents save for college. You can select from two options with these plans. One plan allows you to lock in current tuition rates by purchasing credits. The other plan works similar to any other savings plan in that you just contribute regularly. These plans are only available to be used toward tuition, or room and board. If you withdraw funds from 529s for anything other than college expenses, you’ll be socked with a hefty 10 percent tax.

Work College Savings Into Your Budget: We get it, your paycheck is already a little exhausted when it comes to allocating for retirement, flexible spending accounts and even costs toward your employer’s benefits plan that you’re on. But it’s still important to work some sort of college savings into your budget, even if it’s just $20 a month that you allocate toward a 529 plan or separate savings account.

Savings Bonds: Encourage your family members to gift your child savings bonds on birthdays and for other milestone achievements (i.e. graduation, religious benchmarks, etc.). Savings bonds accrue interest over time and can represent a significant return on investment once they mature, which is usually 15 or 30 years.

Don’t Try to Finance College All by Yourself: While it’s only natural to want to help your children with education expenses, the reality of it is that you may still have to take out student loans in your child’s name. That’s OK, and it’s nothing to be embarrassed by.

How You Don’t Want to Finance Your Child’s College

While we’ve gone over some ideal ways to save for your child’s college expenses, let’s take a look at some options that you should absolutely stay away from:

Credit Cards: Never pay tuition bills with your credit card. Taking on this large of an expense can increase your credit utilization ratio and you’ll likely get socked with much higher interest rates than you would from a student loan if you can’t pay off the balance immediately. You’ll also likely be subject to an additional fee for paying with plastic.

Your 401K: Don’t withdraw money from your 401K to pay for tuition with the pledge of eventually paying it back. In addition to cutting into your retirement funds, you’ll be subject to a hefty tax penalty.

Tips on Saving Money this Back-to-School Season

It’s back to school time! Typically, this is an exciting time of the year (for everyone but students, that is), but even now parents are feeling the pinch because of all the supplies, clothes and other materials their kids need for class. According to the National Retail Foundation, the average household spends about $700 on back to school items, and certainly, this output can significantly increase if your child is heading off to college and is going to need books, a computer, etc. So how do you keep your spending in check and not kill your credit? Here’s a look at some tips:

The Right Way to Back to School Shop

Needs vs. wants: There are things that your kids need and things that your kids want. Try to focus on the “needs” first, and then if your budget warrants it move on to the “wants.” Or you could make your kid pay for their “wants” themselves as a good lesson in financial responsibility.

Shop for deals: Don’t wait until the week before school starts to shop – start now. While many retailers offer back to school sales all month, you might be able to score deep discounts on clothes one week, school supplies the next and electronics the week after that. Browse the ads for sales and shop smart. Beyond this, many states offer “tax-free” days each year, where certain items (including school supplies) are eligible for purchase minus any sales tax. This is another great way to save. Visit www.TaxAdmin.org for more information on this. Does your child need to buy their own textbooks? Try buying them used or rent them off Amazon.com to save.

Try not to carry a credit card balance: Back to school shopping can amount to be a considerable expense. Using a credit card to pay for such a purchase – and then letting the balance carry – can potentially add as much as 50 percent to your back to school purchases. Remember, for the best credit score, you want to try to keep your credit utilization ratio at or below 30 percent. Between interest and the cost of back to school shopping, it would behoove you to pay off your card in full by the due date.

Check for student discounts: If you’re doing more expensive back to school shopping, say like a laptop or tablet from a consumer electronics store, make sure you inquire about a student discount. Many offer student discounts of up to 10 percent. Discounts are also commonly offered on computer software.

Only shop credible websites: If you’re doing back to school shopping online, be wary of having your information stolen. Identity theft is no joke, and certainly, the Internet has empowered a new type of hacking. On that note, make sure that you’re only shopping over a secure Internet connection and only doing business with sites that have a security icon next to the address bar. Additionally, never share your credit card information on a site without “https” at the beginning of its domain. The “s” in “https” stands for “ “security.”

Even if you’re not fully up to speed on the importance and significance of your credit score, you should have some general minimal understanding of just how important that three-digit number is. Yes, you should at least know that it’ll play a role in whether or not you’re approved for a loan as well as the interest rate on said loan. But you might be surprised at the various other ways a credit score can impact your life. While you should always want to qualify for the best interest rates on loans, what we’re about to tell you is even more motivation to whip your credit score into shape.

5 Ways Your Credit Score Can Affect Your Life

Your love life: We’ll kick off this list with arguably the most surprising one. Yes, your credit score may impact your love life. New research shows that when people are evaluating romantic partners these days they tend to choose someone with a similar financial situation. A good situation – and a good credit score – seems to indicate a reliable, trustworthy partner.

Insurance: Poor credit scores don’t just reveal potential unreliability, but research shows that the lower a consumer’s credit score, the more likely they are to file a claim. For this reason, consumers with low credit scores will likely pay higher insurance premiums.

Employment: Are you a finalist for your dream job? Let’s hope you have good credit, too. Though laws vary by state, most employers have the ability to run credit reports on potential employees. Being that good credit scores typically signify trustworthiness, bad credit scores tend to reflect the opposite. According to some reports, nearly half of all employers run credit checks on prospective employees.

Your utilities: You expect water, electricity, and heat at your home, but you may not realize that if your credit is poor, you could be paying more for it. Like we’ve noted in many of the other examples here, if your credit score is low, you’re perceived as more of a risk. The utility companies want their money, and charging higher fees is how they help make up for any possible missed or late payments.

Your apartment: Many people assume that a mortgage is the only living situation-related thing a good credit score is important for. However, if you’re renting an apartment, your landlord will be looking at your score before approving you as a tenant too. That’s because landlords want their money – it’s far better for them than issuing evictions or taking tenants to court. If your credit report indicates a poor history, you’ll likely pay more in rent – if you’re approved at all.

How to Avoid Travel Scams in Summer

Travel fraud and scams are nothing new, but with more and more people using the Internet to book, they are becoming more prevalent. In fact,Forterstates that travel fraud increased by more than 15 percent in 2017 from the previous year. Additionally, some 55 million reservations are made annually on websites posing to be either travel agencies or booking sites. Falling for scams can lead to identity theft, drain your finances and haunt your credit score for years.

So if you’re packing your bags and vacationing this summer, do your best to avoid scams. Here’s how:

Tips for Avoiding Travel Scams

Stick to trustworthy booking sites: Stick to booking your airfare, hotel and rental cars through trusted sites. In addition to the airline- and hotel-specific sites, Expedia, Orbitz, TripAdvisor and Kayak are good ones to peruse for deals.

Book excursions through the hotel/resort: In tourist towns, cab drivers, locals and others will likely approach you offering deals on excursions. Don’t fall for it, as this is a common scam. Only book through your resort or trusted provider.

Beware of cab driver tricks: This is especially true if you’re traveling abroad. Many cab drivers will want to drive you to their travel agent friends or hotels they know. The reality is they’re likely setting you up to be scammed, while they get a kickback on what’s scammed from you for their help. Don’t fall for it. Only book transportation tickets through official offices or websites. The same goes for hotels. Many cab drivers will also try to pull the “my meter is broken” game and charge you an absurd amount for your ride.

Hotel scams: A newer scam is when fraudsters call your hotel room pretending to be with the hotel you’re staying in. They’ll say there was a problem with your credit card and ask you to read your card information to them to verify. Once you hang up, they then have this confidential information. Don’t fall for this, always check in with the front desk in person for any inquiries you receive.

Beware of public WiFi: Some scammers set up WiFi hotspots in tourist-heavy areas pretending to be the official network of the hotel or nearby attractions. The hope is that people will log on for the free WiFi and they’ll be able to swipe confidential info. Check with your hotel for information on their WiFi networks, or just use your cell data to avoid any risk.

How to Maintain a Good Credit Score in College

For high school seniors, spring serves as a rite of passage. It’s a time when boys and girls become young men and women, highlighted by high school graduation and the excitement – for many – of college in the fall. It doesn’t matter whether you’re going away to school or living at home and attending a local university or a community college, there’s a lot of planning that’s involved in the adventure. One that should not be dismissed is planning as it pertains to your financial future.

Yes, we’re talking about building credit and maintaining a good credit score – and there’s arguably no better time to start than the summer before going to college. While you may not think that credit scores matter at 18 years old, falling into bad habits can have a huge impact on your future financial potential.

Why Credit Matters

There are many factors that play into the FICO score calculation. One is credit history, which is why it makes sense to start building it around the time you’re going off to school. Other factors behind a good FICO score include the mix of credit you have, new credit, payment history and debt owed. It’s why now is a great time to apply for that first credit card (if you don’t already have one) and start developing good financial habits. Though there’s a common misconception that a credit score is something that you’ll only have to worry about later on in life, things like student loan interest rates and apartment leases are often at least partially judged by credit score.

Getting that First Credit Card

You should already have a debit card linked to your bank account, but if you don’t have a credit card yet, now is a perfect time to get one. Credit cards are a great way to build credit while you’re in college, and many of the big brands offer good options for students. For cash-strapped college kids, we’d suggest applying for a credit card with no annual fee, good rewards or cash back opportunities on purchases and fraud detection alerts. We’d suggest selecting one credit card and applying for it. Refrain from applying for several at once, as new inquiries can cause your score to take a hit.

Other Tips for Building Credit in College

Building credit in college is all about developing good financial habits, and proper use of your first credit card is great practice. For instance:

Make your payments on time: Payment history accounts for 35 percent of your FICO score, so missed payments that are reported are going to cost you.

Pay off your balance: Try to only use your credit card if you know you’ll be able to pay it off or in the case of emergencies. Minimally, you want to try to only carry a balance of at or less than 30 percent of your total credit limit from month to month. Carrying a balance of anything more than this will lower your credit score.

Some other tips for building credit in college include:

Pay your rent, utilities on time: If you’re staying in the dorm, lodging is configured into your room and board. But if you have an apartment, you’ll likely be on the hook for rent and utility costs. Make sure you pay these on time too, or you risk being evicted or having late payments reported to the credit bureaus.

Check your report: You’re entitled to one free credit report per year from each of the three bureaus, so make sure you get it, understand it and ensure there are no errors on it. If there are errors on your report, dispute them immediately.

Am I Responsible for my Spouse’s Debt after Death?

As if losing a close family member isn’t sad enough, there’s more than just planning a funeral you may have to worry about. In certain circumstances, you could inherit any debt left behind by a deceased relative – something that can really put a dent into your credit score, especially if this was a financial burden you didn’t expect to have to take on. This post is designed to take a closer look at just what happens when a close family member dies and how it could impact your financial well being.

The Estate

When a person passes away, any outstanding debts are paid for by the estate of the deceased. The estate essentially consists of all the money, assets and investments that belonged to the recently deceased individual, with the exception of life insurance money and retirement savings. If the estate has enough to cover any outstanding debt, then the listed beneficiaries will be privy to whatever is left over. If the estate does not have enough to cover all debts, then the estate will be marked as insolvent. If the estate is marked insolvent, creditors have to write it off, as they’ll be unable to collect it and cannot hold anyone else responsible for it.

So how do you possibly factor into this? We examine in the next section.

How You Might be Affected

There are a few ways how you may be responsible for the deceased’s debt:

Joint accounts: If you shared an account with the family member, then by law you’re also responsible for that debt. If you want to close the account down, you’ll first have to settle any amounts owed. Joint accounts are common among spouses.

Co-signing situations: You’re also on the hook for any loans or credit cards that you co-signed on. In this case, you may not have just co-signed on one with your spouse, but with your children perhaps (i.e., student loans, auto loans, etc.) or with a close family member. As is the case with joint accounts, you’re legally obligated to repay any debt in these situations.

Community property states: This is where things can get sticky. If you like in a state designated as a community property state, then you may be held liable for all debts a deceased spouse accrued – even if you didn’t know about or agree to any of it in the first place. Community property designations state that all debts accrued by spouses throughout their marriage are joint – so each individual can be held liable for it. Make sure you understand whether or not your situation qualifies and if you’re residing in a community property state.

Like we said in the opening, it can already be stressful, sad and life-changing on its own when a close family member dies. Throw in potential financial ramifications, and it just becomes even more complicated. Make sure you understand how any potential death could impact you so you’re better prepared if and when it occurs.