Different Types of Credit – How to Maximize Your Score?

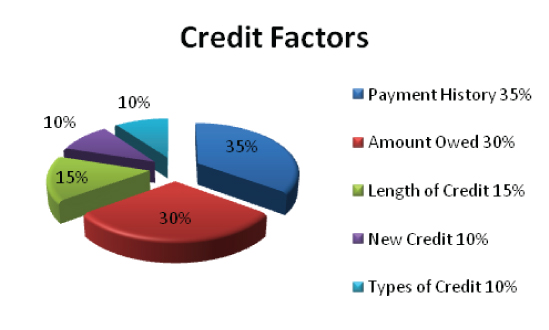

There are five main factors that make up a FICO credit score – payment history, amounts owed, credit history length, new credit and types of credit used.

While the “types of credit” category only factors for about 10 percent of your overall FICO score, it can mean the difference between a good score and a great score, so it’s a category not to overlook if you’re on a mission of credit repair.

First, it’s important to note that there are two main types of finance loans: revolving and installment. Installment loans consist of things like auto loans and student loans — money that is loaned with the expectation that it will be paid back in a relatively short period of time. Revolving loans, which are things like credit cards and bank cards, involve debt that is accrued and, ideally, paid off on a monthly basis (i.e. debt management).

For the best possible credit score, it’s recommended that consumers try to establish a good balance between installment and revolving loans. But here’s a credit tip — there’s one other type of loan that can greatly aid your credit score for the better in the long-term: a mortgage.

When you’re first approved for your mortgage, it’s likely that your credit will take a hit in the near-term. But a mortgage is good for your credit score in the long run for two big reasons. One, it qualifies as a type of credit used. And two, if you make on-time mortgage payments, it will reflect well in the payment history portion of your credit score, which makes up 35 percent of your FICO score.

With all this being said, it’s also worth mentioning that just because you have a variety of installment, revolving and real estate loans to your name doesn’t mean you’ll have a pristine credit score. Like we mentioned above, on-time payments are key. And it’s also key that you don’t have any unpaid loans that are taken on by collection agencies, as it’s hard to repair credit when you have something that could stay on your record — and influence it in a negative way — for up to 7.5 years.

So while diversifying your credit is important, it’s important not to overlook other factors that go into the makeup of your overall score as well.

Cash or Credit – Key Credit Repair Tips and Advice

In order to avoid debt and overspending, many Americans have moved away from credit cards and loans and instead save up cash for purchases. The thinking behind this practice is that they’ll never have to embark on any credit repair or debt management mission, as paying with cash only ensures that they’re never spending beyond their means.

Paying only with cash also ensures that consumers are paying the lowest possible price for items, as they can avoid interest rates that can make large purchases even larger in the long run.

But is paying cash for everything all the time really the right way to go about your finances? While it certainly carries some benefits, one area where this practice can hurt you is how it pertains to your credit score.

Yes, your FICO score, that three digit number that’s essential for getting approved for loans and credit cards and also for cell phone plans, employment opportunities and more. Building credit is important for a variety of reasons, and while many people may be scared off by falling into debt and having to repair credit, a favorable credit score can help you with more than just home and auto loans and credit cards.

Here’s a look at some other reasons why paying cash for everything may not be the best financial strategy:

Your FICO score is composed of five factors: payment history, amounts owed, length of credit history, new credit and types of credit used. If you pay cash for everything, you won’t have a credit report. And while many people are OK with this, there’s the chance of being denied for a credit line in the event of an emergency or being turned away for a job or cell phone plan. Like we mentioned earlier, your credit score is important these days for more than just loan approval and favorable interest rates.

You can have a credit card and be responsible. One argument for paying cash over credit is that you’ll never have to worry about spending getting out of control. But there’s another way to use a credit card and keep spending within means — by being responsible. Here’s a great credit tip to build your score and keep debt down: Make payments on time. Not only does this save on interest, but it’s also the most heavily weighed aspect of your credit score.

So while many are spurning credit cards altogether and opting for a cash-only approach, it’s possible to have the best of both worlds, so your credit score as well as your finances don’t suffer.

Credit Mistakes to Avoid at Any Cost – Credit Tips

Credit Mistakes to Avoid- If you’re in need of credit repair, it’s something that you have to devote time and energy toward working on. Repairing credit takes commitment and a proper understanding of how credit is configured. And while improving your credit score isn’t something that’s easy or fast to do, harming it is something that is.

With that being said, here’s a look at the five most common blunders people make that harm their credit score. Knowing these could be the credit tips you need to keep your score favorable and not poor:

Not paying bills on time: Payment history accounts for 35 percent of your FICO score, specifically if you’ve made on-time payments. A late payment won’t just incur late fees and possibly higher interest rates, but it can immediately dock your credit score of anywhere from 80 to 110 points.

High debt-to-credit ratio: Ideally, it’s recommended that you keep debt-to-credit ratios at about 30 percent for the best possible score. So if you have one credit card and a credit limit of $10,000, keeping it no higher than $3,000 is ideal. Anything more will drop your credit score, so take debt management seriously.

Bad debt: Simply put, don’t let any bills go to collections. Not only will they stay on your credit report for up to 7.5 years, they’re not good for your overall finance picture.

Hard credit pulls: Hard credit pulls are done any time someone is officially approving you for some sort of credit line. They also impact your score by about 5-10 points for every pull and stay on your report for up to two years. Simply put, know the difference between a hard pull, which docks your score, and a soft one, which doesn’t. Many consumers don’t and are surprised to see their score so low.

Check your credit report: You should regularly check your credit report – ideally, once a month. Why? Because it’s estimated that up to 40 million Americans have some sort of mistake on their report. By staying on top of your report, you can monitor and dispute incorrect information, which could be bringing down your credit score.

Closing Out a Credit Card – Does it Damage Your Credit?

So your credit score in unfavorable and you want to get your finances in order. However, credit repair is a big part of getting your FICO score back in favorable order. So what’s there to do?

To put it simply, there is not one tried and true “fix” to turn your credit score from poor to stellar over night. No, instead you need to take a look at the areas where your credit score is lacking luster and then make appropriate changes, whether in regards to debt management, making on-time payments, etc.

But one way people think they can magically improve their credit score quickly is by closing out credit card accounts. This is what we like to call a “repair credit no-no” when it comes to upping your FICO score. Here’s why:

Your FICO score takes into consideration what’s called a “credit utilization ratio.” Simply put, this takes into account your total credit amount versus the amount of credit that is currently being used. Generally speaking, you want to keep this credit utilization ration around 30 percent, meaning that you’re only carrying a balance at or below 30 percent of what your total limit is, for the best possible score.

If you close out a credit card, you’re also eliminating parts of your total credit amount. Say, for example, you have two credit cards. Between the two of them, you’re at a 30 percent credit utilization ratio. You close one of them, thinking it will help, except now your credit utilization amount will rise about 30 percent, hurting your FICO score.

So if someone offers “closing out a credit card” as one of their credit tips, don’t be fooled. The best way to repair credit is to simply make on-time payments, enact debt management strategies to pay down loans and credit card debt and be mindful of the types of accounts you open.

Payment History – Why It’s So Important?

Of the five categories that make up a FICO score, “payment history” is the one that carries the most weight. Specifically, payment history accounts for 35 percent of your total credit score, while amounts owed (30 percent), length of credit history (15 percent), new credit (10 percent) and types of credit used (10 percent) round out the rest of what goes into your score.

But just why is payment history so important? Here’s a look:

The whole point of a credit score is to inform a lender of whether you’re a reliable borrower. And a big part of being a reliable borrower is making on-time payments. That’s the biggest thing that the “payment history” category tells a lender — whether or not on-time payments have been consistently made on things like credit cards, retail accounts and loans.

A common query many consumers have is whether a late payment here or there will harm their credit score. And the answer, in most cases, is no if your score is otherwise favorable. However, if you have regular late payments, credit repair is necessary. Luckily, in this case, it’s simple to repair credit — just make on-time payments.

What’s in the score? Specifically, when it comes to late payments, a FICO score considers not just how many late payments there are, but how late they were, how much was owed and how recently each one occurred.

Like we already noted, the good news regarding the payment history portion of the credit score is that it’s easy to correct. There’s no debt management involved, just the matter of making on-time payments. So take these credit tips from us as it pertains to your finances. Make sure your credit history is in check. It’s the biggest piece of the FICO pie.

FICO Factors: What’s in Your Credit Score?

Whether it’s getting approved for a home loan, car loan or car insurance, your credit score plays a big role. And the score that creditors check most frequently is the FICO score. Needless to say, credit is confusing to a lot of people – and if you don’t know what goes into the makeup of a credit score,

just how do you know whether you have good credit or are in need of credit repair?

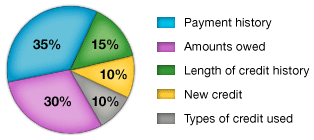

With that in mind, here’s a look at the five factors that are used to determine one’s FICO score. We call it “the FICO 5”:

Payment History: Payment history accounts for 35 percent of your FICO score – the single largest category. Simply put, have you paid all your past credit accounts on time? If you have, then you’re good in this area. If you haven’t, then you’ll likely take a hit in this category and have to work to repair credit.

Amounts Owed: This factor accounts for 30 percent of your FICO score. When you borrow money, you’re given a credit limit. This factor takes a look at how close you are to using all your available credit. The closer you are, the more your score will suffer.

Credit History Length: This represents 15 percent of your FICO score. The longer your credit has been established, the better it is for you and your score.

New Credit: Ten percent of your total score, this reflects any new sources of credit you’ve opened recently, as several recently opened accounts pose a greater risk to lenders.

Types of Credit: The final 10 percent of your FICO score, this category factors in your credit cards, retail accounts, loans and every other source of credit.

As you can see, there’s a lot that goes into your FICO score, which is why it’s important to be on top of all the various categories and to practice good debt management strategies, as your credit score could determine what you can and cannot finance.

Bad Credit Score – It Hurts!

Everyone knows that a good credit score is essential to getting approval for everything from car insurance to car loans—and for getting the best possible interest rate that’s currently being offered—but what many people don’t seem to realize is just how much of a toll a poor FICO score can have on you.

So if you have a poor score, it’s important to take it seriously and enact credit repair, whether it means deploying debt management techniques or implementing good bill-paying habits. Here’s a look at how a poor credit score can hurt you and your finances.

High credit card interest rates: Credit cards are notorious for the high interest rates they charge. After all, it is how the card companies make their money. However, if you have poor credit, you can anticipate paying 22 percent and upward, should you even be approved. That’s a far cry from the 10 to 19 percent that’s likely with a good score.

Loan interest: How much more can you expect to pay on a car loan with a poor credit score? Possibly up to 2 whole percentage points of interest! Mortgage loans, too, can mean you that you will have to pay potentially tens of thousands more over the course of a loan with a poor score. Repair credit, and take it seriously to avoid these preventable expenses.

Miscellaneous: Can you imaging trying to sign up for a cell phone plan only to find out at the store that you’re ineligible because your credit score isn’t good enough? It happens. The same goes with car insurance. Presently, 47 states are permitted to check your credit score to determine the rate.

As you can see, a poor credit score can really hurt! So if yours isn’t satisfactory, make sure you’re taking the proper steps to correct it.

More Insurance Tips

Understanding General Insurance coverage: Suggestion For The Smart Consumer

When it comes to dealing with insurance coverage, it may seem like it is you versus the globe in some cases. With the huge quantity of information available online, it can be almost overwhelming at. This article will certainly offer much practical info for you to obtain begun on the appropriate course.

When you make any sort of improvements to your house that price over a specific amount, you should make sure to call your insurance company and allow them find out about it. If requirement be, many insurance carriers make you state renovations to them that cost a lot so that your plan can be readjusted.

Keep your broker or insurance firm updated on anything that may affect your policy or protection. If they do, then they could propose the next program of activity in concerns to your insurance coverage plan.

When you decide on insurance coverage for your auto, certify your insurer. Evaluating protection, it is additionally in your best passion to look for evaluations on their client solution, case responsiveness and also also rate increases. Understanding which you are dealing with ahead of time can aid you set assumptions with your insurance firm.

Commonly, you will want to get in touch with other client testimonials of specific insurance policy business just before spending your cash in their policies. By speaking with sites like Angie’s listing as well as other such customer remarks, you can acquire a sense of the current popular opinion towards an insurance policy business. If the majority of the firm’s patrons are pleased, that may aid you develop a choice, and also vice-versa.

Have your insurance coverage company reconsiders your scores if your credit history rating has gone up. Insurance business do base component of your preliminary premium on your credit report. Without your consent though, they could just inspect it when they initially supply you protection unless you have had a lapse of insurance coverage. If you know your credit has risen, having your credit rating reconsidered could possibly bag you a reduction in your costs.

When comparing insurance business, the wise customer will certainly take their own loyalty right into account. An insurer that has supplied years of reliable, hassle-free and also reputable service need to not be deserted the instant a slightly more affordable different becomes available. It is fairly most likely that an insurance firm that provides rock-bottom prices is cutting corners somewhere in the solution they provide their clients.

An annual review of their insurance plan is a routine every person ought to exercise. Make certain that all details on your plan is correct and also update it with any type of adjustments. See to it you are receiving credit report for such points as automated seat belts on your automobile policy and safety surveillance on your property owner policy.

In summary, you would like to do all that you can to learn concerning insurance policy. There is a lot of information available, yet we have given a few of the most essential pointers. Ideally we have supplied you with sufficient details to not only provide you a strong background, however additionally further spark your passion to come to be a professional in it.

If they do, then they could recommend the following course of action in regards to your insurance policy. Typically, you will certainly want to speak with other consumer assessments of certain insurance coverage companies just before investing your cash in their plans. If your credit history rating has gone up, have your insurance provider company rechecks your ratings. Insurance policy firms do base part of your initial premium on your credit rating rating. An annual testimonial of their insurance policies is a routine every person need to engage in.

Business Credit – How Does it Work?

If you’re a start-up company, chances are you’re going to be falling back a lot on your personal credit in the early days of your operations. And while that’s perfectly normal, your goal as a business owner shouldn’t be just to grow your business over time but to grow it in a way that you can also build business credit.

What is it though? It’s similar to your personal credit score, except from a business perspective. For instance, while your personal credit score is important, your business score should be kept separate in order to increase your company’s financing ability and credit capacity. This helps a business acquire the likes of equipment, office space, loans and financing and anything else that is pertinent to current and future operations. And it’s important to build business credit because starting a business can be a real struggle at times, potentially exhausting any personal credit options. By building a good business FICO score, you’ve now got another avenue to draw from.

Establishing

We already mentioned how it works very similarly to personal credit. So in order to build it, you’ll have to borrow money, repay the borrowed money responsibly and make sure that the payments are reported to a credit reporting bureau. But just like your personal credit, your business score isn’t something that’s built overnight. In fact, just like your personal score, one of the key factors that lenders often look at when analyzing what type of a borrower you are is the length of your credit history. That’s why it’s important to begin to establish business credit immediately after you start your company.

As a reminder, your business credit is not the same thing as personal credit, so don’t treat them the same way. Apply for business credit under a Tax Identification Number, not your personal social security number, and make sure you’re meeting all the federal and state guidelines for operating a business within a given area. One other thing that can help your business score is incorporating your business. Incorporating helps limit personal risk, which can make you a more qualified borrower and increase your credit score. It’s not uncommon for many businesses to incorporate as part of a credit repair plan.

Benefits

There are three big benefits of business credit: a big credit capacity, to increase company value and to protect your personal credit. Here’s a closer look at these three key benefits:

Large credit capacity: It’s estimated that successful businesses can have up to 100 times more of a credit limit than a personal credit score. This alone gives a company a lot of latitude to pursue new ventures and increase revenue within the business.

Increase company value: The better the credit score, the more attractive a company becomes, not only in terms of increased revenue but in terms of how it looks to potential investors and potential buyers.

Protect personal credit: As previously noted, being able to rely solely on your business credit for company matters helps protect your personal credit score, keeping the two entities separate. It’s not uncommon for new businesses to rely on one’s personal credit in the early days until an adequate enough amount of business credit can be built, but ideally, there’s a separation of church and state between a personal credit score and the business part. It’s best for business owners and the business.

Tips-Build Business Credit.

So now that you know a little bit about business credit and why it’s important to build it, just how can you go about doing it? Here’s a look at some tips and pointers for getting your business credit score up:

Start a business bank account: One of the first things you should do as a new business is open up a bank account. Banks report to the credit bureaus, so it helps start a line of credit. And opening up a business account will help you keep business and personal matters separate.

Don’t let your personal credit score slip: Business and personal credit scores are not the same, but you still shouldn’t let your personal credit score slip. That’s because in the early days of your company when your credit is still being built, it’s likely that you’ll be viewed as more of a high-risk borrower when applying for loans. Because of this, it’s not uncommon for the bank to grant the loan and rest liability with the owner on a personal basis. In order for a bank or lender to do this, the personal credit score needs to be adequate. So it’s important not to give up on the personal credit score, as in such cases it’s important to also build your credit for your business.

Be responsible: Responsibility is the key to building good credit. Make sure all bills are paid on time; monitor your credit score as you begin to grow it; and even consider consulting with a credit expert to help you and your business in the early days.

What is a Good Credit Score?

Good Credit Score – It behooves you to have a good credit score. Why? Because a good credit score is key to borrowing money – whether it be for a car loan, home mortgage or some other type of loan – with low interest rates. A poor credit score, on the other hand, may disqualify you from qualifying from a loan or stick you with a high interest rate. Bottom line – the better your credit score, the more favorable borrower you are.

So with that in mind, just what is a good credit score? And when should you repair credit?

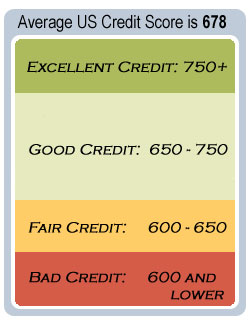

To answer that question, let’s take a look at the FICO score, the score that the majority of lenders use to determine borrower risk. Specifically, the FICO score ranges from 301 to 850. Here’s a breakdown of the ranges that most lenders use to assess risk in a nutshell:

750+: Anything at 750 or better is considered excellent credit. A borrower should be able to get approved with the lowest possible interest rates on loans with this score.

700-749: Scores in this range are considered “good” and should lead to approval with low – if not the lowest available – interest rates.

650-699: This range is considered “fair.” And while borrowers can still get approved in this range, they may end up paying a higher interest rate.

600-649: The range between 600 and 649 is considered poor credit. Credit scores in this range may jeopardize loan approval. If approval is granted, borrowers may have to pay significantly higher interest rates from someone with good or excellent credit.

599 and below: This is considered bad credit.

As you can see, the higher the credit score, the better you’re viewed as a borrower. Should your score fall below 700, credit repair measures are often recommended.

Errors on My Credit Report – How to Fix?

You’re applying for a big loan soon, and before you do, you’re doing due diligence with your credit. You check out your report… and don’t recognize many of the items listed in it. “What’s going on?” you’re thinking. You don’t recall some of this stuff.

Errors on My Credit Report Are you going crazy ?

Likely, no. In fact, errors are more frequent than you may realize when it comes to credit reports and your credit score. According to estimates, about a quarter of all credit reports that have been surveyed by the U.S. PIRG have contained serious errors.

Furthermore, about 80 percent of all credit reports surveyed contained at least one minor error.

If your credit report is revealing some incorrect information, what do you do? This is especially important if the report is impacting your FICO score to the point where credit repair is necessary. Here’s a look:

Know whether the information in question is actually incorrect. This may seem like an elementary point, but if you have no way to justify this, you’ll have no case.

Dispute it. Once you know something is wrong, contact the party (i.e., lender, collection agency) that is reporting the information. You may also elect to contact the credit agency reporting the information. Start by asking them to fix it. If that doesn’t work, then disputing it is the next step. Typically, you can accomplish this online or via mail. Disputing online is quick, but you’re able to be much more thorough when disputing through the mail, as you can include the relevant documentation to get the issue resolved.

After submitting your dispute, then you play the waiting game. If you don’t hear anything after one month, follow up with the appropriate parties. If your dispute is successful, all three credit reporting bureaus must be informed of the error.

So if something doesn’t look right on your credit report, don’t automatically assume that you need to repair credit. First, look to see if there are any errors. About 80 percent of credit reports are found to have one.