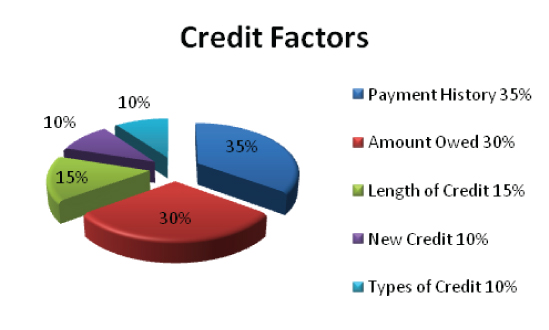

Of the five categories that make up a FICO score, “payment history” is the one that carries the most weight. Specifically, payment history accounts for 35 percent of your total credit score, while amounts owed (30 percent), length of credit history (15 percent), new credit (10 percent) and types of credit used (10 percent) round out the rest of what goes into your score.

But just why is payment history so important? Here’s a look:

The whole point of a credit score is to inform a lender of whether you’re a reliable borrower. And a big part of being a reliable borrower is making on-time payments. That’s the biggest thing that the “payment history” category tells a lender — whether or not on-time payments have been consistently made on things like credit cards, retail accounts and loans.

A common query many consumers have is whether a late payment here or there will harm their credit score. And the answer, in most cases, is no if your score is otherwise favorable. However, if you have regular late payments, credit repair is necessary. Luckily, in this case, it’s simple to repair credit — just make on-time payments.

What’s in the score? Specifically, when it comes to late payments, a FICO score considers not just how many late payments there are, but how late they were, how much was owed and how recently each one occurred.

Like we already noted, the good news regarding the payment history portion of the credit score is that it’s easy to correct. There’s no debt management involved, just the matter of making on-time payments. So take these credit tips from us as it pertains to your finances. Make sure your credit history is in check. It’s the biggest piece of the FICO pie.

Bad Credit Score – It Hurts!

Everyone knows that a good credit score is essential to getting approval for everything from car insurance to car loans—and for getting the best possible interest rate that’s currently being offered—but what many people don’t seem to realize is just how much of a toll a poor FICO score can have on you.

So if you have a poor score, it’s important to take it seriously and enact credit repair, whether it means deploying debt management techniques or implementing good bill-paying habits. Here’s a look at how a poor credit score can hurt you and your finances.

High credit card interest rates: Credit cards are notorious for the high interest rates they charge. After all, it is how the card companies make their money. However, if you have poor credit, you can anticipate paying 22 percent and upward, should you even be approved. That’s a far cry from the 10 to 19 percent that’s likely with a good score.

Loan interest: How much more can you expect to pay on a car loan with a poor credit score? Possibly up to 2 whole percentage points of interest! Mortgage loans, too, can mean you that you will have to pay potentially tens of thousands more over the course of a loan with a poor score. Repair credit, and take it seriously to avoid these preventable expenses.

Miscellaneous: Can you imaging trying to sign up for a cell phone plan only to find out at the store that you’re ineligible because your credit score isn’t good enough? It happens. The same goes with car insurance. Presently, 47 states are permitted to check your credit score to determine the rate.

As you can see, a poor credit score can really hurt! So if yours isn’t satisfactory, make sure you’re taking the proper steps to correct it.

More Insurance Tips

Understanding General Insurance coverage: Suggestion For The Smart Consumer

When it comes to dealing with insurance coverage, it may seem like it is you versus the globe in some cases. With the huge quantity of information available online, it can be almost overwhelming at. This article will certainly offer much practical info for you to obtain begun on the appropriate course.

When you make any sort of improvements to your house that price over a specific amount, you should make sure to call your insurance company and allow them find out about it. If requirement be, many insurance carriers make you state renovations to them that cost a lot so that your plan can be readjusted.

Keep your broker or insurance firm updated on anything that may affect your policy or protection. If they do, then they could propose the next program of activity in concerns to your insurance coverage plan.

When you decide on insurance coverage for your auto, certify your insurer. Evaluating protection, it is additionally in your best passion to look for evaluations on their client solution, case responsiveness and also also rate increases. Understanding which you are dealing with ahead of time can aid you set assumptions with your insurance firm.

Commonly, you will want to get in touch with other client testimonials of specific insurance policy business just before spending your cash in their policies. By speaking with sites like Angie’s listing as well as other such customer remarks, you can acquire a sense of the current popular opinion towards an insurance policy business. If the majority of the firm’s patrons are pleased, that may aid you develop a choice, and also vice-versa.

Have your insurance coverage company reconsiders your scores if your credit history rating has gone up. Insurance business do base component of your preliminary premium on your credit report. Without your consent though, they could just inspect it when they initially supply you protection unless you have had a lapse of insurance coverage. If you know your credit has risen, having your credit rating reconsidered could possibly bag you a reduction in your costs.

When comparing insurance business, the wise customer will certainly take their own loyalty right into account. An insurer that has supplied years of reliable, hassle-free and also reputable service need to not be deserted the instant a slightly more affordable different becomes available. It is fairly most likely that an insurance firm that provides rock-bottom prices is cutting corners somewhere in the solution they provide their clients.

An annual review of their insurance plan is a routine every person ought to exercise. Make certain that all details on your plan is correct and also update it with any type of adjustments. See to it you are receiving credit report for such points as automated seat belts on your automobile policy and safety surveillance on your property owner policy.

In summary, you would like to do all that you can to learn concerning insurance policy. There is a lot of information available, yet we have given a few of the most essential pointers. Ideally we have supplied you with sufficient details to not only provide you a strong background, however additionally further spark your passion to come to be a professional in it.

If they do, then they could recommend the following course of action in regards to your insurance policy. Typically, you will certainly want to speak with other consumer assessments of certain insurance coverage companies just before investing your cash in their plans. If your credit history rating has gone up, have your insurance provider company rechecks your ratings. Insurance policy firms do base part of your initial premium on your credit rating rating. An annual testimonial of their insurance policies is a routine every person need to engage in.

Credit and Finance Around the World – 10 Things You May Not Know

If you go to Europe, your favorite credit card may not work. In Norway, you need to enter a PIN for all credit card transactions. In other parts of Europe, cards are now implanted with EMV chips for security.

Throughout the continent of Africa, merchants and ATM owners are held financially responsible for fraud. (In the US, the card issuer is the one that’s left, legally, holding the bag.) As a result, 77% of credit card systems on that continent require the extra security of EMV chips.

In Kenya and Tansania, most minor financing transactions don’t go through a bank. They are handled with a mobile system called M-Pesa that is run by the countries’ two largest mobile phone carriers.

Chances are that Americans lag people from other countries in financial literacy. The Organization for Economic Cooperation and Development has begun testing 15-year-olds to find out how much, on average, kids from each country know. The results of the financial literacy test won’t be out till later this year; however, US scores are currently below average in math, which tends to correlate with scores in financial literacy.

In Scotland, Northern Ireland and Wales, math teachers are required to have units on financial literacy in their classes. England and Australia will be adding this requirement to their curriculum as well starting with the 2014 school year.

A new US company, COIN, is recruiting customers for the launch of a digital credit card wallet. The new system will be a substitute for the eight or more cards most Americans carry every day.

In Canada and Australia, the average consumer charges over $7,000 on credit cards every year. That’s almost double the average American’s charges of around $4,000. Canada has over 72 million credit cards in circulation, compared to 686 million in the US.

Countries where people use credit cards less tend to have higher savings rates. In Germany and France, the average consumer charges just a few hundred dollars a year. The average savings rate in both countries is over 10% of income per year.

About half of all Americans carry a balance on their credit cards. By contrast, over three-quarters of South Koreans pay off their balance in full every month.

In many countries where credit card usage is low, even large transactions are handled in cash. For instance, expenses associated with a wedding in Turkey or Bahrain would be paid in cash, despite being thousands of dollars.