00:01 Guys, what’s up? I just parked my car at the office, and, um, I just got off a phone call with a client, okay? Uh, a client that I’m absolutely totally stoked for. A client of mine called me last week and said Nick, I’ve got $27,000. I’ve saved 27 grand, $27,000, guys. This is not a small task, okay, but here’s the dilemma. I got $27,000 in credit card debt. What the heck do I do? Do I pay off the debt or do I keep the money in the bank?

00:35 Short answer, pay off the debt. Are you insane? Are you nuts? Are you crazy, okay? Get rid of that money. Get rid of that money, pay off that debt, and guys, it’s simple math. The bank’s giving you zero percent. They’re giving you nothing. You stick it in the bank. I get it, it’s nice. You stick it in the bank. You’ve worked hard. You’ve saved. You’ve done the right things to budget, okay, while you’ve been paying the minimum payments on your credit cards. I get it. You hit that number. It’s in the bank, but they’re giving you nothing. But, they’re turning around and they’re charging you 15%, 20%, 25, 30%, okay? These are insane rates. The equation is broken. You’re getting zero percent from the bank and they’re turning around and lending it to you at 29%. There’s something wrong with that, and you’re going to say, well Nick, I’ve been told cash is king. I need to have the cash handy.

01:26 Guys, you have to have faith. That’s what you need. You need faith, number one, that’s it’s gonna be okay to not have that $27,000, and for you guys that are used to servicing debt, you service debt, you pay the minimum payments, you got an Excel spreadsheet where you just monitor your debt. It’s not your friend, okay. Don’t get comfortable with it. They’re sucking the money out of your pocket and you don’t even realize it’s happening, okay? You’re going to be fine when you have less money in the bank, okay, you’re left with a few hundred books or a thousand dollars if you follow the Dave Ramsey system, which I love. Um, you’re going to be fine. Why? Because when you have less resources, you become more resourceful.

02:05 We’ve all been there. We’ve all been dead broke. None of us had an anxiety attack from being dead broke. But, if you walk into the ER, I guarantee there are plenty of people walking in there every single day that are having panic attacks and anxiety attacks because of the calls they’re getting from their creditors. I promise you, it’s a packed house and I know this, because I get about 100 calls a minute at Key Credit Repair with these exact same scenarios. You gotta have faith. The numbers make sense guys. Take the cash, pay off the debt. Get rid of the rates, okay? And then guess what? You’re going to be able to accelerate your savings pretty substantially, because now all that cash that’s coming in baby, you’re not servicing debt anymore. Okay? You want to spend it? Do whatever you want, okay? But you’re not sending it off to banks and lenders, because they’re going to spend it, okay?

02:51 Um, and again, you gotta have faith that it’s going to be okay. You’ve all been at rock bottom before guys, you’ve all been at zero. We’ve all been there. Let’s say we, and we’ve survived. Why? We had faith. See you guys, this is Nik Tsoukales with Key Credit Repair. By the way, to that client that just paid off $27,000 in credit card debts, you are the man. You are the man. I love you for doing that. And if you are having this dilemma or a debt dilemma, call me guys. My direct line is 617-326-3685. We have about 15 consultants on staff that deal with these issues all day long. But I want to hear from you. If you get my voicemail, leave me a message, let me know that you just paid off a debt. Even if it’s a small debt, leave me that message. Email me, Nik@Keycreditrepair.com.

03:40 Let me know that you’re having this dilemma. If you feel like you don’t necessarily have the faith, you feel like you’re feeling, you’re feeling a little weak. I’m not sure if I should pay off the debts, hit me up guys. Let me re-encourage you. I’ve been there personally, okay? That’s why I feel so passionate about what I do, okay? So let me re-encourage you, let me show you the way. Let’s get out of debt, let’s use our money to get wealthy. Let’s grow our credit scores. Let’s use credit to build wealth, and let’s absolutely crush it. Later guys.

Should I use my savings to pay off debt?

Utility Bills – do they show up on my credit report?

Your Credit Minute Show Notes:

00:01 YouTubers, what’s going on? This is Nik Tsoukales with Key Credit Repair. So I want to talk to you guys today about utility bills. Check this out, actually. I will show you, I got my electric bill today, okay? So, it kind of inspired me to talk about utility bills. So, big question I get all the time is does my electric bill, do my utility bills report to credit? 99% of the time, they don’t.

00:23 There are a few markets like Detroit, Michigan, specifically, um, DTE, um, where you will find, uh, your ongoing utility bill’s going to report to the three credit agencies, okay? It’s not very common though, okay? Most of the time, they will not, okay? But what will report to the credit agencies very quickly is a defaulted, uh, utility bill.

00:47 So let’s say you don’t pay your electric bill and it falls 90 days behind. The utility companies are super sophisticated with this, their systems will auto batch that data to the credit agencies and all of a sudden you have a 50, a 100, a $500.00 collection that dings your credit report. I’ve seen some people with absolutely perfect credit. They make great money. There’s no financial hardship. There’s no inability to pay.

01:11 There really even, there really even isn’t a question of credibility, but they miss a utility bill, they’re on vacation, all of a sudden their credit is pretty much totally destroyed, um, from a credit score perspective, or they’re losing a quick hundred points. Um, that is something that can be remedied by paying off the debt very quickly, reaching out to the utility company and asking them to lift it from your credit report.

01:32 If they’re not willing to, which I would say 75% of the time they’re not going to be willing to, that’s a phone call that you definitely want to make to us and we can help you and approach a strategy on how to get the actual record deleted from the credit report. Guys, this is Nik Tsoukales with your quick credit minute. Have an amazing day, and thanks for checking us out every day. Bye.

Utility Bills – do they show up on my credit report?

Build Credit – So you wanna know how to build credit

Your Credit Minute Show Notes:

00:01 YouTubers, what’s goin’ on?

00:03 So you wanna know how to build credit. I get it. You’re new. You’re brand new to credit.

00:08 Or you’ve taken a credit hit over the years, and you’re just making your financial comeback. You haven’t used credit in a while.

00:15 Or you’re just new to the country and you wanna know, “How do I re-establish credit?”

00:18 Well let’s show you. I’m gonna jump on the whiteboard real quick, guys. Let’s jump on the white board real quick, and let’s do this together, okay? And let’s show you how to build up some credit.

00:29 Okay, remember the rule of three, guys. Most banks and lenders, well, what do they wanna see? They wanna see that you have at least three active trade lines on your credit report. So what’s Nick’s rule of three? Um, or what’s Nick’s strategy, in terms of an actual, and if you’ve ever done a consultation with us, is three active trade lines. That’s mandatory, that’s how many we wanna have on the credit report.

00:48 So the first thing you wanna do is make a note. Grab a notebook, grab a piece of paper.

00:53 By the way, a credit action plan should only encompass one piece of paper. It does not require a notebook. Don’t waste your money on notebooks. Grab a sheet of paper, okay?

01:01 Um, so we want the rule of three, okay? We want a good mix of “Revolving,” “Installment,” okay, and then eventually “Real Estate Credit.”

01:12 Why? ‘Cause 15 percent of the credit score is types of credit, having a healthy mix of different types of credit, okay? Um, but in this case, to build credit, obviously, we’re not gonna get real estate credit, okay? My suggest is one credit card, two credit cards, okay, and one secured loan, okay? Let’s talk about this.

01:43 Now, the question you’re gonna ask is, “Nick, how do I get a credit card when I don’t have credit?” Okay, it’s pretty simple actually. Something called a secured credit card, okay?

01:52 You can go to a website called bankrate.com, I don’t know if you guys can read this. Bankrate.com

02:02 So bankrate.com is gonna give you a list, there’s actually a drop-down in the credit card selection section where you can search credit cards, where you can search starter credit cards and secured credit cards.

02:13 The concept of a secured credit card is fairly simple, okay? You’re going to take $500, okay, and you are going to put that $500 or give that $500 to the credit card company, okay? They’re gonna hold that $ 500 as collateral, okay? It’s collateral. This is not a prepaid credit card. This is collateral. They’re just holding it, okay?

02:38 And what they will then do, in turn, is issue you a credit card with a $500 credit limit, sometimes a little lower as well. Sometimes a little higher.

02:47 Why do they do this?

02:48 Well, they have no risk. You have no credit, so you’re considered a higher risk for them, especially when you’re re-establishing credit, okay? But when you’re putting up that collateral, there’s no risk. If you don’t pay on that credit card and you go into default, guess what? They’re gonna take your money.

03:02 Now, the good thing is, a lot of these secured credit cards, after you’ve established credit, they’ll offer you unsecured credit cards, and you can actually get your security depots released. Some of them will do it, um, right up front, they’ll actually tell you, in six months of on-time payments, they will release, uh, that security, okay?

03:20 So we wanna get two of these secured credit cards, okay? And then we want to get a secured loan.

03:27 So, remember, we want a good, healthy mix of active accounts. We have revolving accounts, which are credit cards. We have installment accounts, which are personal loans, student loans, or car loans. But again, the dilemma is, we don’t have credit, how are we gonna get these things?

03:41 Well, this same concept here, with the secured credit card, where you put $500 into a, um … or you give it to the bank as collateral and they give you a credit line for $500, you can actually do that with an installment loan. Usually they’re a little pricier, okay? Most banks will do it for about a thousand dollars in the form of a CD. So they’re gonna take that thousand dollars, and they’re gonna put it into a certificate of deposit, okay? Don’t get caught up in the fancy talk, it’s a savings account, okay? But the savings account is locked, typically for a 6, 12, 24, 36 month period, okay?

04:20 They will then, in turn, give you … we’ll go over here, we need a little space … a loan for a thousand dollars. They will give you … remember what we talked about? Having a mix of different types of trade lines? They will give you an installment loan for a thousand bucks, okay?

04:37 So there we go, guys. We got a credit card, our two secured credit cards, then we have a secured loan, okay? We have that healthy mix of three active trade lines. We’ve done it without a credit score, okay? Most of your local banks, lenders, um, credit unions will offer you these two products. Secured credit card, secured installment loan.

04:58 If you need any help, or you need some direction on where to access the-these types of products, um, we have full access to all this stuff in our client portal if you Sign Up for $0 Today with us. Um, aside from that, you can access through our blog. We have a million and one resources. You can actually reach out to one of our consultants, um, Sign Up for $0. We’ll actually direct you on where to go to get these products.

05:18 Guys, this is Nick Chucales. This is Rebuilding Your Credit 101, and if you have any questions, give us a call. Bye.

Build Credit- So you wanna know how to build credit

Consumer Credit Counseling – Why I love this program!

Your Credit Minute Show Notes:

00:00 What’s up, YouTubers? So, for those of you that are looking for a way to get out of debt, okay, obviously we’re not a debt relief company here, but a lot of our clients and a lot of inquiries we get here are looking for this type of help. So, I’m gonna give you an example of one program that I’m a big, big fan of and I’m gonna break down really what it is, give you the kind of, the bare bones um, or kind of the structure of what it is and then I’ll uh, make some suggestions in terms of if maybe that’s the right program for you. So, what we’re gonna talk about today is something called CCC. Another acronym. [inaudible 00:00:34]. Consumer Credit Counseling, guys. Consumer Credit Counseling I think is one of the better programs out there to help you get out of debt. Why? Number one, it is credit score neutral. Doesn’t hurt your credit score. Okay? Um, you’re not required to fall behind on the debts. Okay? It’s not a settlement program, it’s not a debt relief program. It’s a way to get out of debt. It’s a money management system. It’s a budgeting system.

01:01 So, let me break down for you really kinda how it works because it’s pretty simple stuff actually. Okay? Let’s make a little room here. So, you owe a bunch of debt. Okay? You owe a Amex for $20,000. You owe a Capital One for $10,000. You owe, I don’t know, Visa o- Walmart for $5,000. Okay? So, you have $35,000 in credit card debt right now. Okay? You’re in this debt, you can’t get out of it, you’re not sure what to do. Okay? Also, you got minimum payments of $1,500 baby. Interest (laughs) only. Guess what? Every time you send that $1,500 none of it’s going towards principal. So, you’re stuck. You’re just literally burning $1,500 every month. Why? Because uh, you were five minutes late on making these payments one month. And, guess what? Your interest rate’s 30% on this, 28% on that, 18% on this. And, keep in mind, these are fictitious and examples, okay? Don’t quote me exactly. But, your interest rates are super, absolutely insane sky high. So, you got, you’re sending $1,500 right now and you’re just kinda sending it out into the wind. Okay? So, how do we remedy this?

02:22 Okay, well, Consumer Credit Counseling might be the way. So, Consumer Credit Counseling agencies are typically nonprofit organizations. They’re nonprofit organizations, okay? Um, they should be fully licensed in the state that you live in to do business there. Usually, you are able to meet with someone face to face locally to sit down and do one of these programs as well. So, keep that I mind when you’re doing a Consumer Credit Counseling program. Okay? And, usually what the CCC is going to do is they’re gonna meet with you and they’re gonna come up with a budget. Okay? First thing they’re gonna do is they’re gonna say, how much do you make? Income. What are your expenses? Okay? Typically, the income is the issue. Most people that have gotten ems- gotten themselves into debt and qualified for CCC are people that have either had their hours cut at work, they’ve lost a job, or a spouse has lost a job. Okay? So, when they fill out one of these budgets, they’re gonna notice that. And, they’re gonna see that by, quickly, your expenses have gone up since then as well because, guess what? Um, the interest rates have gone up on all your credit cards too, so you just can’t afford this. Okay?

03:24 What they’re gonna do, and typically what they already have arranged um, is interest rate deductions. Okay? So, you see these 30- 30% interest rates? These are gonna get reduced. Okay? Usually, the CCC has arrangements with Amex, with Capital One, with Walmart card, or whatever they’re gonna be. Okay? And, they have arrangements with them that if someone does fall behind, they come through one of these programs and they’re gonna offer you a lower interest rate, as long as the CCC is managing the disbursement of the payment. So, let’s say right away they approve you for a CCC program and you get all your interest rates down to a fixed 5%. Okay? Um, but, let’s say you can still continue making this $1,500 payment. Well, instead of this having the interest only, all of a sudden, you know, you got $1,200 out of the $1,500 quickly going towards principal. So, what does that do? It really just drives down these amounts. The principal balance here, uh, they start to drop pretty significantly pretty quickly and you start getting yourself out of debt. Okay? Other times, the payment is just so outrageous um, that you can’t afford this at all. So, they’ll actually reduce the payment. They’ll get you back on your feet.

04:33 That way you have a little free money to put towards um, to put towards paying these things down, and really just quite simply to, to live and survive at this point, until you get that next job. What’s nice about this is it is credit score neutral. Okay? But, keep in mind, there will be a comment on your credit. Okay? There’s a comment section on the credit report. Okay? And, it will say something along the lines of managed by a CCC, Consumer Credit Counseling agency. Okay? That comments there, it’s a credit s- uh, it’s a credit score neutral comment. Okay? But, it’s placed there so if you try to get some credit card debt while you’re in one of these programs, they’re not gonna approve you. They’re gonna see the comments um, and they’re not gonna give you a new loan, which it really isn’t something you should be worrying about, you know, if you’re in debt and you’re trying to get more debt, don’t complain about that. It’s not a big deal. Okay? Um, also what’s nice is the disbursement. So, instead of you making payments to each of these creditors every month, they’re gonna do it for you.

05:40 So, this is you. Happy, happy, joy, joy. Okay? And, you’re gonna be sending money to the Consumer Credit Counseling agency um, each month and they will then do the disbursements. Okay? Um, the CCA will do the disbursements for you every single month. So, you’ll only have to pay one company each month. The companies will not be calling you. They’re not gonna bug you. They’re not gonna harass you. Um, it really makes life a lot easier. You have kind of a, an extra layer of protection from your creditors. Okay? So, Consumer Credit Counseling guys, um, check out some Consumer Credit Counseling agencies. You can check out the Better Business Bureau, bbb.org. You can find a list of them local to you. I would advocate you try to get into the Consumer Credit Counseling agency’s office if they have one local. If they don’t have one near you, not the end of the world, but I think there’s a huge benefit um, you know, sitting down with the agent, going through the budget together, and really taking a hard look at what your finances are. Guys, this is Nikitas Tsoukales with Key Credit Repair, and have a great day.

FCRA – What is the fair credit reporting act and why does it matter?

Your Credit Minute Show Notes:

00:00 What’s up, YouTubers? This is Nik Tsoukales with Key Credit Repair, and today we’re gonna talk about one of my favorite things in the world; FCRA.

00:08 FCRA, FCRA, FCRA. We talk about FCRA a lot here at Key Credit Repair, and if you’re wondering what FCRA, well, let me introduce you to, let me introduce to FCRA. We got the Fair Credit Reporting Act.

00:23 This is the fuel. This is what allows us to repair credit. This is what allows you to challenge things on your credit report. This is something that sets the United States apart from, um, really from everyone. There’s a reason why our system is set up in a way where we get a restart button, we can protect ourselves. Um, we have the Fair Credit Reporting Act. Okay.

00:43 There’s a reason why credit repair’s so prevalent in the United States, you can challenge things because we have rights enacted by Congress that allow us to challenge something negative on a credit report.

00:52 So, I’m gonna give you just some basic facts, but then I’m gonna talk about why this is super beneficial.

01:00 So, if you can read my bad handwriting here as always, ah, the Fair Credit Reporting Act, enacted by Congress in 1970. Okay.

01:05 And these are some of your basic rights. You have the right to know. You have the right to know what’s on your credit report. Okay. Um, someone can’t mask that information, they can’t hide it from you. If they’ve used that data to make a credit decision and you’ve been declined, they have to share that with you.

01:21 Okay. You have the right to a credit score. So, if you’ve been recently declined for something you probably got the letter in the mail referencing the Fair Credit Reporting Act and giving you a credit score, and also a range of credit scores depending on the type of credit score that’s used. They have to give that to you by law. Okay.

01:36 Then you have the big one, a right to dispute. Anything inaccurate, incomplete, unverifiable or really just questionable, you have the right to challenge on the credit report. So, it doesn’t need to stay there because it was placed there, otherwise I’d be out of a day job, right guys?

01:53 Um, also, last but not least, the right to legal action. So, if you send a dispute letter off to the credit agencies and you’re challenging something that’s just obviously inaccurate and they refuse to remove it or properly investigate it, you have the right to legal action. You have the right to take these guys to court, you have the right, um, to get paid, ah, to get, to get paid for damages. Okay. So, keep that in mind.

02:16 This is the leverage that you have when you’re doing credit repair. Okay.

02:20 Also, the FCRA is, um, something that is, um, administered and monitored by the Federal Trade Commission. Okay. So, we have a government agency that oversees this. You also have the Consumer Financial Protection Bureau that’s heavily involved in making sure that no one violates the FCRA anymore. Um, and also you have advocacy groups like Key Credit Repair and other credit repair companies that can help you challenge things that could be an obvious violation of the Fair Credit Reporting Act.

02:45 Now, keep in mind there’s gonna be a follow-up video to this explaining FDCPA, another fancy acronym we use here a lot, which is the Fair Debt Collections Practices Act. So, for those of you with that, that’s gonna be the acronym that you wanna follow, especially if it’s questionable debt.

03:01 The Fair Credit Reporting Act is quite clear. Also keep in mind with the FCRA, something to think about is, you know, you have the right to challenge these things but it doesn’t have to be vague. Okay. And when I say vague it means we have some clear guidelines for how long these companies have to respond.

03:19 So, when you send out a dispute letter, you’ll probably hear the rule of thumb that we have 30 days, we have 30 days for an investigation. Where does this 30 days come from? Well, it’s actually in the Fair Credit Reporting Act. Okay.

03:33 I’m gonna supply the link for you guys, um, to Wikipedia, okay, where you can actually see a history of the Fair Credit Reporting Act, see why it was created and why. Okay, you can see some of the furnisher information, um, some of the uses of consumer credit reports, of permissible purposes as well. Okay. So, someone just can’t pull a credit report because, ah, they want to. They have to have permissible purpose.

03:54 So, I’m gonna list that out for you, as well as giving you a link for a free PDF download at, um, keycreditrepair.com/credit-laws. Okay. You can actually download a full PDF version of the Fair Credit Reporting Act. Especially for you, for those do-it-yourselfers, if you wanna get some ammunition when you’re, when you’re creating those letters, you can get them right there.

04:16 Thanks guys. This is Nik Tsoukales with Key Credit Repair. Have a great day.

Home Loan – What credit score is used in your application?

Your Credit Minute Show Notes:

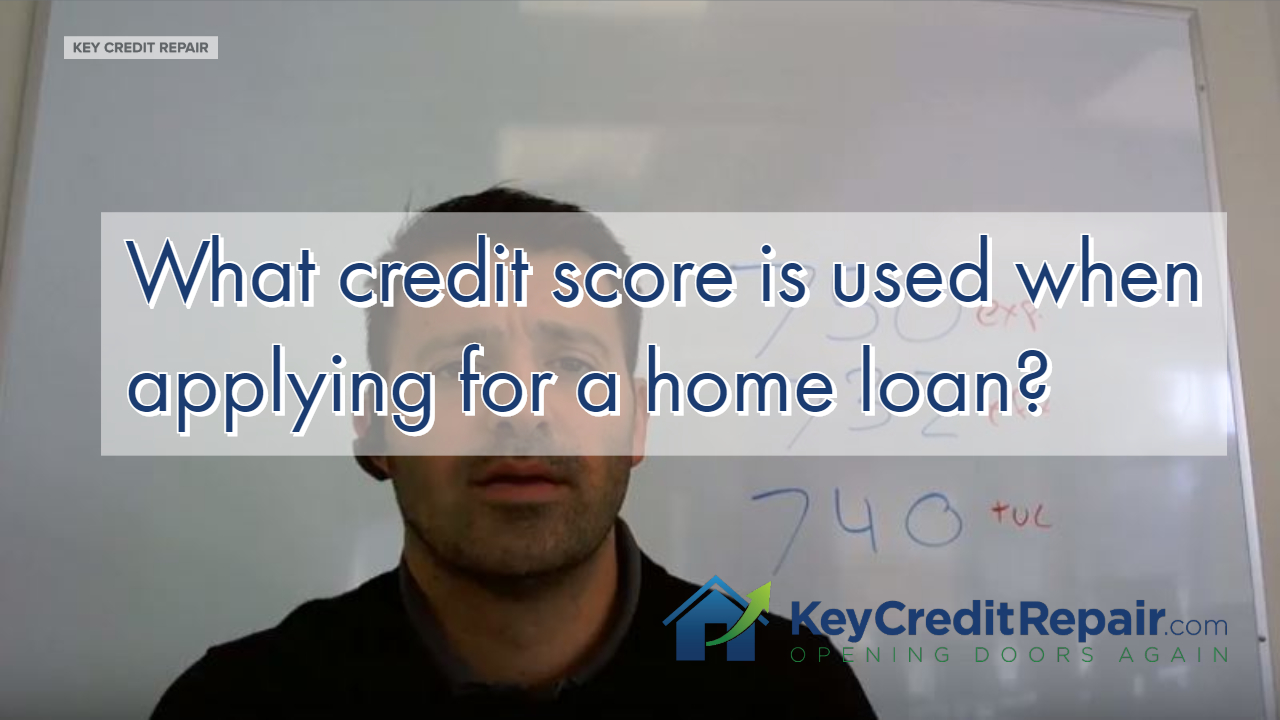

00:00 What’s up YouTubers, this is Nick Tsoukales with Key Credit Repair. And today’s credit question of the day is gonna be “Which credit score is used when I am applying for a home loan?” So pretty simple stuff, okay.

00:10 So let’s say for example we have a 750 credit score for Experian, okay. We have a 732 for Equifax, and then we have a 740 TransUnion, okay. A lot of people are gonna think, well Nick, it’s the middle credit score. Well, it sometimes is the middle credit score, so that’s not entirely incorrect, but in this case, the middle credit score would have been a 732, which is technically the lowest credit score, okay. So it’s definitely not the 732, okay. I mean it’s definitely not the lowest credit score, and it’s definitely not the highest credit score. A home loan um or a mortgage lender is gonna use something called the median credit score, or middle of three values. So in this case, what you’re gonna look at is you’re gonna stack up the three credit scores, okay. And you’re gonna look for middle of three values. So in this case, we have 740. So this is obviously the lowest, this is the highest, and this is the middle of three values.

01:01 So again guys, if you’re pulling your credit score, wondering which one is used for a home loan, it’s always gonna be the middle of three values. The credit score that you need for a home loan is always gonna be a FICO score, and the place to get that FICO score, aside from a mortgage lender is gonna be myfico.com.

01:15 Guys have a great day.

Does Debt Settlement Hurt Your Credit Score?

Your Credit Minute Show Notes:

00:01 YouTubers, what’s up? This is Nick Tsoukales with Key Credit Repair. Today we are talking about debt settlements. So the big question that we’re getting asked all the time is debt settlement, de-debt relief. Is it, is it hurting my score? Will it hurt my credit score? So let’s actually break down what a debt relief plan is, what debt settlement is, how it happens, and whether or not it hurts your credit score, okay?

00:23 So typically a debt settlement plan, okay, is a plan where you are going to start setting aside a certain amount of money into a special purposes savings account, okay? Now with the savings account, as the money starts building up, okay, that money that-that savings, okay, is gonna start being used to settle each of your debts, okay.

00:50 Now what are the major pros with a program like this? Well the first big thing is the savings, okay. Now let’s say you have a ten thousand dollar debt, okay. The debt settlement company typically is gonna negotiate a pretty aggressive settlement with this company, okay. So let’s say we have a debt collector, okay. Um that-that settling company is technically is going to be settling the debt somewhere between four and six thousand dollars, or somewhere between forty and sixty percent, so you have major savings.

01:28 Now what is the downside, um with a debt settlement plan? Okay, well really there isn’t. As long as you’re in collections. So let’s say you-you’ve already fallen behind on all of your … uh on all of your accounts, okay? You’ve gone through some hardships and all of these accounts are currently in collection status. Paying the off through a settlement, bringing them to zero is going to help your credit score. It’s a positive thing for your credit, okay. These accounts are already in default.

01:55 Now let’s say these accounts are all up to date, and you fall behind, okay. You go ninety, a hundred and twenty days late, to use that at leverage to possibly negotiate a settlement, something like this later on, obviously that’s gonna have a damaging affect on your credit score, okay. Keep in mind guys, we talked about this, thirty five percent of your credit score is payment history. So the second you go ahead and you fall behind on those debts, that thirty five percent is gonna be affected pretty dramatically. We’ve seen clients go from 750 to 550 in one month from falling behind on all of their accounts.

02:32 Now if you’re looking to file for bankruptcy, this is an alternative, okay. This is a a great alternative, okay. Also, let’s break down why this can actually happen. Okay? Typically when these debts go ninety to a hundred and twenty days behind, these debts are gonna get sent over to a collection department at a bank, okay. They will start aggressively reaching out to you to try to get you to pay on the debt, okay. Usually you can get something off with each of those accounts, so if it’s a ten thousand dollar debt, maybe you’re gonna get a couple thousand dollars off, okay. But if some additional time passes by, those debts are then gonna get sold, okay. And when they get sold, this is where you can start saving the bucks. Okay.

03:17 A ten thousand dollar debt, a credit card, okay, is typically sold to a collection agency for about a thousand bucks, I’m not kidding you. Ten cents on the dollar, okay. Now keep in mind, a lot of these debts never get collected, okay. So they’re usually not gonna give you a thousand dollar settlement. But when you end up paying them back-

03:42 Sometimes you don’t.

03:42 Five thousand dollars, or fifty percent, okay, it works out for everyone. The collection agency made some money, technically. They’ve made four thousand dollars, okay. They’ve recovered some money from you for all the debts they’re not gonna collect, for all the people that are filing for bankruptcy, you’ve saved a ton of money, um they make some money, everyone is happy. The original creditor up here um they took a write off on the loss, okay. So they took a tax deduction for their loss as well, so it all works out well in the end for everybody.

04:16 But again, if you’re up to date on these debts guys, a debt relief program is something you’ve really gotta think about. It should only be deemed as something to avoid bankruptcy, um if the debts are-have already fallen behind, um whether you paid it off in full or settling the debt, it’s a net positive, the account is already in default, it’s already in negative balance, bringing it up to date in any way shape or form can only help you.

04:38 Guys this is Nick Tsoukales from Key Credit Repair, thanks for checking out our uh our YouTube channel and our Facebook channel, um everyday we’re producing uh new content regarding credit. If you have any questions that you’d like me to answer, you can email me at info@keycreditrepair.com. Thank you.

Credit Score Range- How do I stack up?

Your Credit Minute Show Notes:

00:01 Hey, guys. This is Nik Tsoukales with Key Credit Repair. I’m taking you through a quick credit minute talking about the different credit score ranges. So, I’m going to break it down in three different ways for you. Okay.

00:11 The first credit score that we have is something called the Vantage score. Vantage score 3.0 or 4.0. Okay. Then, we have your FICO score. Um, typically what you’re seeing online is FICO 8 and FICO 9, and then I’m going to give you an additional FICO score as a bonus round. This has a little house on it, and I’m going to explain in a second why this matters.

00:40 So, the first thing we’re going to talk about is the Vantage score. Okay. What is a Vantage score? Where do you get it? Okay. Vantage score is the credit score you’re going to find on creditkarma.com. It’s a free credit score that you can access. Okay. The Vantage score is owned by the three credit agencies. It’s owned by TransUnion, Experian, and Equifax. Okay. Um, it is an educational purposes only credit score. Most banks and lenders don’t use it, but for the purpose of credit repair, monitoring your credit, it’s a really good range.

01:11 So, I’m going to actually read off some notes here for you guys and give you the exact break down directly from FICO in terms of where we should be. Okay. So, to me directly from Vantage score. So, you have, okay, let’s see. We’re going to go from 300 to 600, that is considered a poor credit score in their eyes. Okay. Then, you’re going to have 601 to 660, which is considered a fair credit score. Okay. Then, we’re going to go 661 through 780, which they consider good, and then 780 plus, which they consider excellent.

02:04 Now, keep in mind, this is for educational purposes only. So, if you’re in these ranges, um, you’re doing pretty good. If you’re in this range, you’re really doing amazing. Okay. Uh, let’s move on to FICO score. Okay.

02:23 So, one of the most commonly found FICO scores online for educational purposes only is FICO score 8.0 or 9. Okay. And, their range is going to be fairly similar with a few exceptions. 300 to 579 is going to be what they consider as poor, and then we’re going to say 580 to, let’s see here, 669, and by the way I’m going to show you in a second why I could care less what they say. This is an important part of this. I could care less what these numbers are. 670 through 739 is considered good. 740 plus is considered excellent. Okay. And, by the way, this score caps out at 850.

03:22 Now, I could care less what Vantage score says is a good credit score or a bad credit score, and I could care less what FICO score or FICO 8 says is a good or bad credit score. So, we’re going to go ahead and we’re going to throw all of this out. We could care less. What we care about is what we can get with our credit scores, and most of my clients are trying to eventually buy a home, and if you’re buying a home, you’re not using either of those two credit scores. Those are just for educational purposes only.

03:48 What we care about is another [inaudible 00:03:53] FICO. We’re going to call this the house FICO score. Okay. So, when you go to get a mortgage, uh, the mortgage lenders going to pull something called a trimerge credit report. Okay. That data- When they pull that data in, they’re going to push it through, uh, the FICO algorithm and issue you a score, okay, but the way the scores presented to you is going to vary between the three bureaus. Okay. So, you could have the exact same data between all three bureaus, and there’s a variation natural algorithm that’s used that’s why no three credit scores are exactly the same. Interesting stuff here.

04:32 Experian, they’re using a version two. Okay. Equifax is using- using version five, and TransUnion is using version four. If you’ve ever heard of a Beacon score, guys … Some of your old school bankers will know this. They’ll say, “Hey, what’s your Beacon score?”. Okay. In the old days, your Equifax credit score was called a Beacon score. Now, these credit scores are all from FICO. Okay. These are the scores that matter. This is what the banks and lenders are using.

05:05 Now, let’s talk about the ranges. In terms of what is considered good or bad, I mean, it’s kind of arbitrary. What I care about is what I can access with my credit score. Okay. So, I’m going to give you a few numbers to focus on. 640, 680, and 740. Okay. Goal number one, goal number two, and goal number three. Okay. Now, obviously, these scores range from about 300 to 850, but again we could care less about that.

05:35 What I care about is this … 640 is a goal number one for the majority of my clients. Why? Because that’s going to allow them to access most, um, FHA back loans. So, essentially, you’re getting a house around 640. Now, there are some banks and lenders that will go lower than that. They’ll go to 600 or even 580, but there’s usually contingencies and more complicating factors that they want to get you that loan, but 640 you’re- you’re in. You’re approved. You’re getting something pending all the other things are- are working out in your favor. Okay.

06:04 680 is just about the national average. Okay. I care about that. I want to know that I’m at least average. I don’t want to be below average. Okay. Also, that’s technically the beginning of most conventional findings. Conventional findings means basically what they’re not looking for the Federal Housing Administration, conventional money. Uh, they’re not looking for the Federal Housing Administration to back your mortgage. Okay. So, usually the rates, the fees are going to be lower. Okay. You’re just going straight to the bank. They’re saying, “Hey, you’re- you’re average. You’re making a living. Let’s give you a regular loan”. Okay.

06:42 And, then 740. 740 is considered really that crème de la crème at the bank level. When they see a 740 plus at that FICO score, that Beacon 5.0, that FICO two or that version four, that’s a credit score that’s going to get you the lowest interest rates. That’s what you’re going to be able to really competitively shop from one bank to another. That’s when you’re getting the best interest rates on things like credit cards, the zero percent APR offers, zero percent on a Cadillac for 12 months offer, all that good stuff. That’s where you want to be.

07:15 So, regardless of what a website is telling you guys. Good, fair, bad, excellent, green light, red light, 10 stars or none, we can care less. What we care about is what is your credit score getting us? Is it getting us a house? If not, then who cares. Guys, this is Nik Tsoukales with Key Credit Repair and this is your credit minute. Have a great day.

Free Credit Report-How do I get one?

Your Credit Minute Show Notes:

00:00 What’s up, YouTubers. Today, we’re gonna talk about a subject that we, uh, we talk about a lot here at Key Credit Repair, and it’s probably one of the most searched, uh, credit queries on Google, and it’s, uh, and excuse my bad handwriting, uh, free credit report. Okay. Where do I get my free credit report? How do I get one? What website do I go to, or you think you’re getting a free credit report, but actually you’re not, so let’s talk about free credit reports, guys.

00:28 So, I’m gonna give you guys where you can get your free credit report, how to get it, what the catches are, what the gimmicks are, because, trust me, there are a lot of them. Okay.

00:41 So, what’s the deal with these credit reports? Well, number one, the United States government has allowed you, the consumer, access to your credit reports through the three credit agencies, once per year, for free, unless you’ve recently been declined, which you can actually request them again. Okay?

00:56 Now, where do you access this? Well, technically speaking, there’s only one website. There’s only one, guys, where you can access all three credit agencies completely free of charge, but I’m gonna give you the catch. Okay? So, that website is going to be annualcreditreport.com. Okay. Annualcreditreport.com. Okay.

01:24 Now, when you get to this website, it’s gonna give you the ability to pull your Equifax, okay, your TransUnion, and your Experian credit data. Okay. You’re gonna get everything. Every nook and cranny of that data, you can get once per year for free. You can download it as a PDF. You’ll have access to it forever and ever. Okay. It’s a great thing, and it’s extremely detailed.

01:46 Once again, what’s the catch, though? The catch is no one said in any of these laws that your credit score is free. There’s no credit score. Okay. No score. Okay. Now, there is the option, through each of the bureaus when you’re, when you’re accessing that free data, to upgrade and pay somewhere between eight and ten bucks per credit score, okay, but if you’re just looking for the data, you wanna see what’s on there, it’s very much recommended. Okay.

02:14 Now, if you wanna go one step further, you wanna get some of your data or as much data as you can, plus credit scores, okay, or some sort of credit score, and you have another site that’s super popular these days, and one we tend to recommend a lot because we like how usable it is, and you have Credit Karma. Okay. Credit Karma’s gonna allow you to access your TransUnion credit data 100% free of charge, okay, your Equifax credit data, and you’re not getting your Experian data. That’s one of the catches. Okay. Also, you are getting credit scores in the form of something called a Vantage Score. Okay. So a Vantage score is a credit score that’s used for educational purposes only. It was created by the three credit agencies. It’s owned by the three credit agencies. Banks and lenders do not use it. 90% of credit decisions are made using what? FICO scores. So Credit Karma’s a good report. We like the monitoring. We like it, but realize you’re not getting everything. Okay. You pay for what you get, and you’re not paying anything here, so you don’t get everything. Okay.

03:28 The other website that we like is freecreditreport.com, but another catch. Here’s the other catch, guys. It’s freecreditreport.com or freecreditscore.com. You are only getting free Experian data. Okay. Equifax, you get nothing. TransUnion, zero, zip, zilch. Okay. And, usually, you’re gonna get some sort of a score. Um, I’ve seen them offer FICO or usually FICO 8 or 9, which banks and lenders, of course, they’re not using it yet. Most mortgage companies using FICO 4 or FICO 5, um, or they’re using their plus score. Okay.

04:27 So, if you want the free data, just the data, annualcreditreport.com. Okay. You can get an upgrade and you can pay for it to access scores, but there are no scores. Credit Karma’s gonna give you TransUnion, Equifax, and a Vantage score, which is really good for educational purposes only. Um, you get a free app, as well, and the credit monitoring alerts are really good. Okay. Um, another thing negative with Credit Karma, something I don’t like is the fact that I’m constantly being marketed. Okay. Keep in mind they’re not charging you anything. They need to make money. So, every time you log in, guess what? There’s a banner for Amex, there’s a banner for Visa, there’s a banner for this, that, and the other, and I don’t like the fact that my data is out there in that way, although it’s out there anyway somewhere, right? Um, and then we have freecreditreport.com, which is giving you Experian data, plus one credit score. Okay.

05:15 Now, that’s where you’re getting some free credit reporting. Now, what is the common theme here? If you want it all, you must pay. Okay.

05:29 One thing I tell every single one of my clients, “Stop being cheap. Pay for credit monitoring. You will pay for all types of warranties, all types of things. You will pay all types of counselors, advisors, and coaches, but you will not shell out 20 or 30 bucks per month, $360 per year, to monitor all three of your credit agencies, to check all three of your credit agencies, and to look at and monitor all three of your credit scores.” That’s financial insanity. Okay.

05:58 If you wanna look at exactly what the banks are, uh, and lenders are looking at at all times and you’re willing to shell out the cash, and credit is important to you, then my suggestion, and you guys will see this a lot, this is not for cheap people, is myfico.com. Get on there. I think their three-in-one membership right now is somewhere in the ballpark of 30 bucks. All three credit agencies, all three FICO scores in every variation of the FICO score. Remember, guys? FICO 4, FICO 5, banks and lenders, mortgage companies, that’s what they’re using. FICO 8, FICO 9, they’re not using it. We could care less if we’re getting that score for free. Um, you also have auto lending scores, credit card scores, insurance scores. You got everything on there.

06:46 So, guys, that is your explanation about free credit reports. All right? This is Nik Tsoukales with Key Credit Repair, and this was your credit news for the day.

Good-Will Intervention-Asking Nicely will Help Improve your Credit.

Your Credit Minute Show Notes:

00:00 What’s up guys? This is Nik Tsoukales with Key Credit Repair. Today we’re going to talk about something a little outside of the box, something a lot of people really aren’t talking about in the credit repair field, um, and it really is a creative way to help you start repairing your credit. Okay?

00:15 So, obviously, we get the question a lot. “Late payments. Late payments. What do I do with my late payments? I can’t get them off. I can’t get them removed.” Um, well there is a way to get this done. Okay? Keep in mind, one of those ways is by challenging the data. Okay? Is it verifiable? Is it accurate? If it’s not, it’s gotta go. Okay? Being persistent with your attempt at getting these things removed when they can’t be verified, when it’s garbage. Okay? The item shouldn’t be on your credit report.

00:44 Well, let’s say, you’ve have some siter, some sort of minor blip with a company. Okay? They placed the late payment on your credit report, but really is more for technical reasons that it was late. Maybe one of their systems wasn’t working, but the account did, in fact, go late. You don’t have much you can necessarily challenge. Well, what do you do then? Okay. The, we got a question, actually, yesterday from a client who’s dealing with some student loans in this way. Where there’s really more of a technical issue that created the lates.

01:09 The lates were, in fact, lates. Okay? The money didn’t get to them on time. But really, should that affect their credibility? And that was kind of a question mark? Um, also, this outright disputing the account really hasn’t worked, um, for this client. They’ve actually attempted to do it themselves. And they wondered what is a plan B? And that’s what I want to lay out for you guys, which is something, again, a little outside the box. Okay?

01:35 And what we’re going to talk about here is something called a good will intervention. Okay. We are taught to fight, we are taught to never surrender, we are taught to go after the big, bad credit agencies and our creditors. We’re taught to take ’em down, right? But you don’t always have to. Sometimes, you can actually ask nicely. Okay? If you’ve had a really good run with a creditor, um, a bank, a lender, everything’s been going well, but because of some sort of technical issue or something really in the gray, a late was incurred, okay, you don’t necessarily need to challenge their record. What you can do is you can challenge the creditor to be nice to you, in the form of something called a good will intervention.

02:22 And what a good will intervention really is, asking the creditor to remove the late out of their good will. Okay? Understanding that the issue was really technical and has nothing to do with your credibility. Okay. This is an option in the way we help clients all the time, when the late isn’t something they really agree with, but it’s not necessarily black and white. Where instead of just challenging the record, disputing it outright, when that’s really not the way to do it, um, we’re asking the creditor politely, “Hey, can you make this adjustment? This didn’t, in fact, uh, uh, really feel like it should be a late payment, and it’s something that’s really fallen into a gray area.”

02:57 So a good will intervention is a great way to approach this. And it’s extremely effective. And, if a company’s doing really good business with you, okay, and you’ve been a client of theirs for a long, long time, they’re really going to want to help expedite you. They’re really going to want to help, uh, accommodate you when, uh, when a mistake like this happens, from whether it’s their fault or yours, long as your in agreeance that you were, uh, actually, in fact, able to make that payment, um, and that there is not effect in terms of credibility here.

03:25 So good will intervention is going to be the way to go, guys. There’s a lot that goes into this, so keep in mind, something you definitely want to speak to one of our credit experts about. I really wouldn’t go at this specific approach alone, okay? Letters gotta be written a certain way, um, you want to appeal to them a certain way, so I would definitely, um, this is not one of those do-it-yourselfer tips. I would reach out to one of our credit experts. You can click on one of the links below. There’s probably a few consultation link below, or learn more link below, if this is on Facebook. Or you can check us out at keycreditrepair.com\freeconsultation. Give us a call. Ask specifically about the approach with the good will intervention, and we’ll discuss it with you and see if that’s actually something, uh, that is an option for you. Because we don’t want to just start doing this stuff blind.

04:11 Guys, this is Nik Tsoukales with Key Credit Repair. Have a great day.